India Tightens Crypto Oversight: 49 Exchanges Registered, Unregistered Ones Grow

Alex Smith

5 months ago

The Indian government continues to take stricter steps to regulate cryptocurrency transactions, with many platforms coming under tougher regulation to combat money laundering and other illicit practices using cryptocurrencies.

As reported by official sources, nearly 50 cryptocurrency exchanges registered themselves with India’s Financial Intelligence Unit in the 2024-25 fiscal year, out of which 45 are in India and four are abroad.

Exchanges Register With FIU

The registrations make the exchanges reporting entities under the Prevention of Money Laundering Act. They are now required to file Suspicious Transaction Reports, identify wallet beneficiaries, and disclose bank accounts and platform contact details to the FIU. These steps aim to make it easier for authorities to trace large or unusual flows of funds.

49 crypto exchanges are already FIU registered, and 100s more that are not.

The crypto market in India is far more competitive than most people think.

IMO, Healthy competition is good for the ecosystem as it promotes innovation https://t.co/5BAS86eBEh

— Sumit Gupta (CoinDCX) (@smtgpt) January 6, 2026

Regulatory Action And Penalties

Last year saw concrete enforcement. Regulators imposed fines totaling about ₹28 crore on non-compliant platforms during FY 2024–25, a figure that media reports have translated to roughly $3.1 million. At the same time, the FIU issued notices and ordered blocks against a group of offshore platforms that had failed to register or meet anti-money-laundering obligations.

Authorities say the move followed strategic analysis of Suspicious Transaction Reports that flagged patterns of misuse. Reported red flags included hawala-style transfers, gambling and fraud schemes, instances tied to darknet services, and links to terror financing and child sexual abuse material. Those findings helped shape the decision to escalate oversight and enforcement.

Offshore Platforms TargetedThe FIU sent notices to and ordered the takedown of access for a list of about 25 offshore exchanges that were serving Indian users without registering. Several mainstream news outlets and legal newsletters named platforms such as BitMEX, LBank, Paxful, CEX.IO and others among those targeted. These actions used powers under the Prevention of Money-Laundering Act and the Information Technology Act to block apps and web access in India.

For traders and savers, the drift is clear: expect stricter KYC checks and closer monitoring of transfers between wallets and bank accounts. Registered exchanges will likely have more compliance steps and reporting duties. That can mean extra paperwork and, in some cases, higher costs as platforms absorb compliance expenses. At the same time, users who rely on unregistered overseas platforms risk losing access if those services are blocked domestically.

Featured image from Unsplash, chart from TradingView

Related Articles

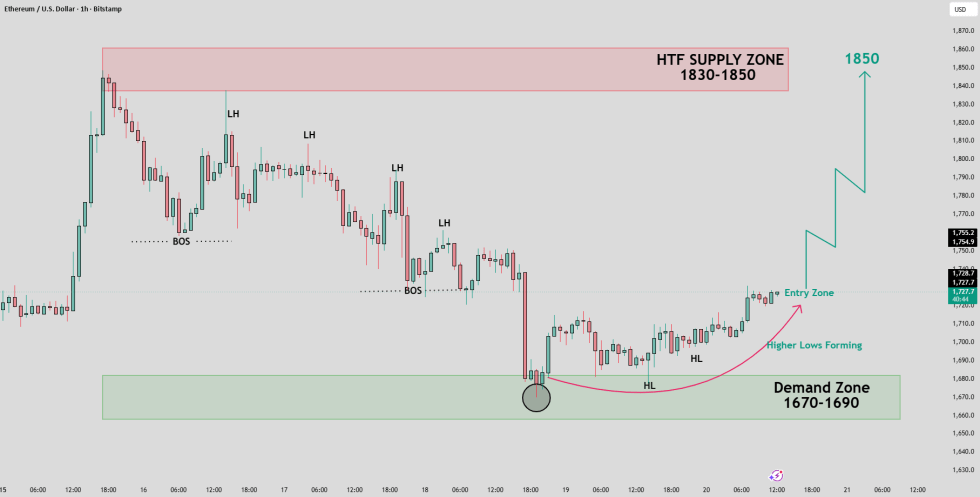

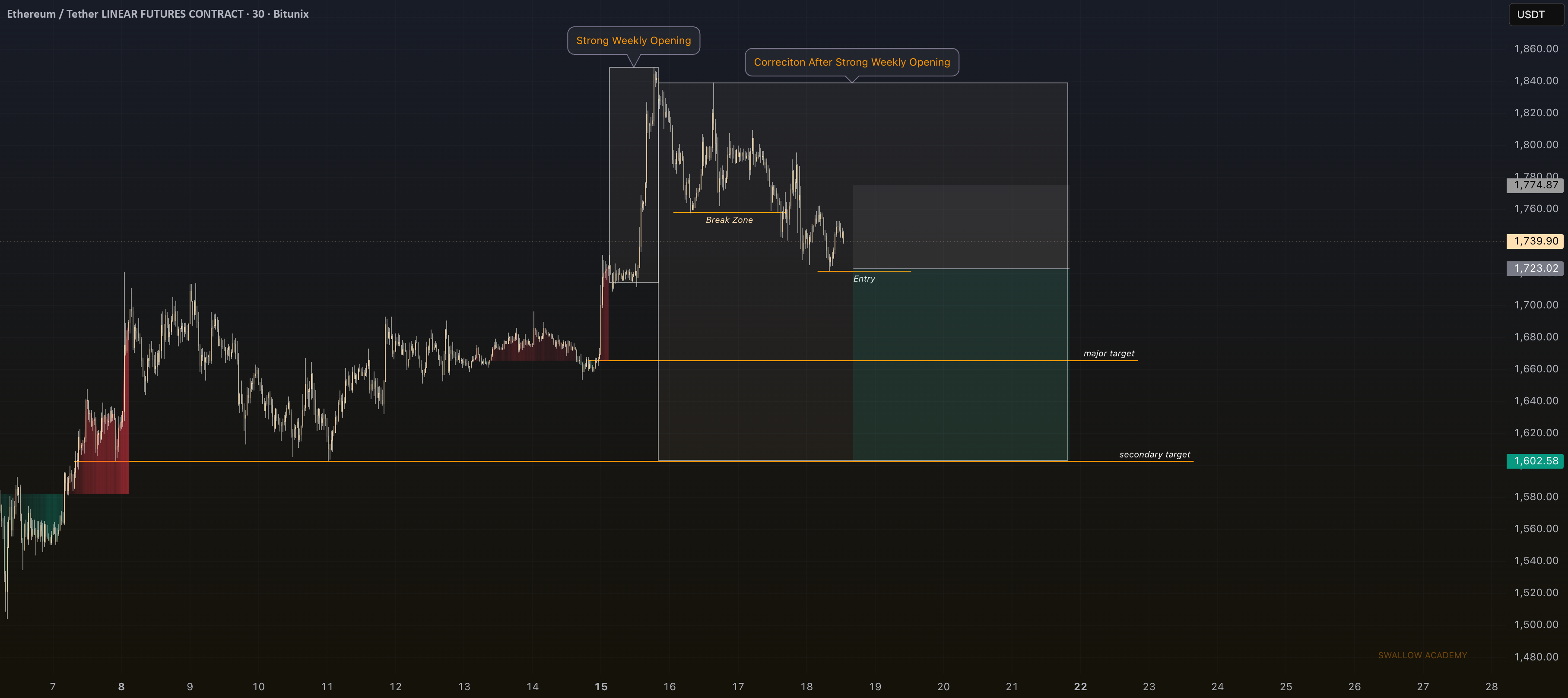

Ethereum Price Setup Targets $1,850 As Buyers Defend Key Demand Zone

A TradingView analyst says Ethereum could target $1,850 if buyers defend the $1,...

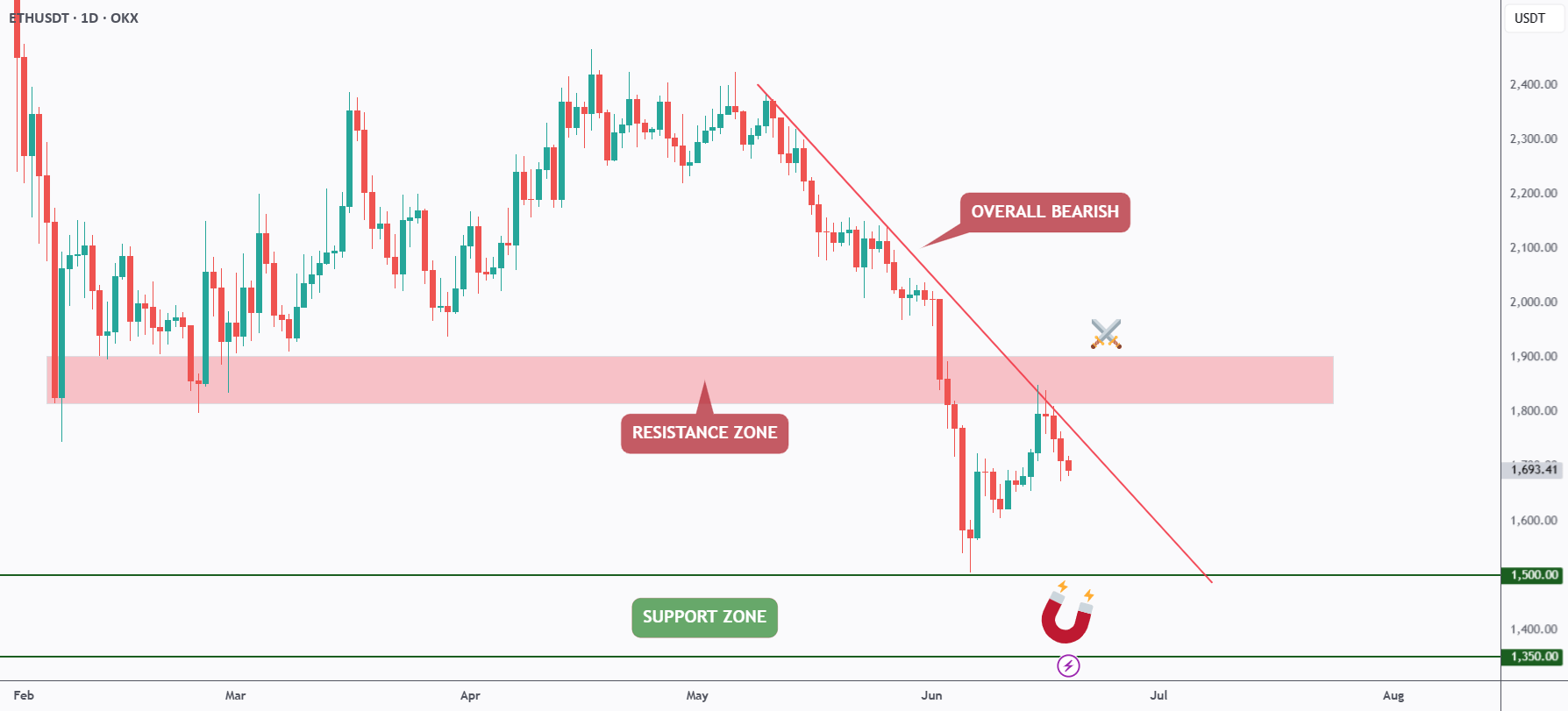

Ethereum Bears Keep Control As ETH Rejects Trendline Resistance

A TradingView analyst says Ethereum remains bearish below a falling trendline, w...

ETH/BTC Ratio Falls Back To Early-2023 Levels As Traders Debate Ethereum Value

An X analyst says ETH/BTC is back near 0.027, while a TradingView chart shows ET...

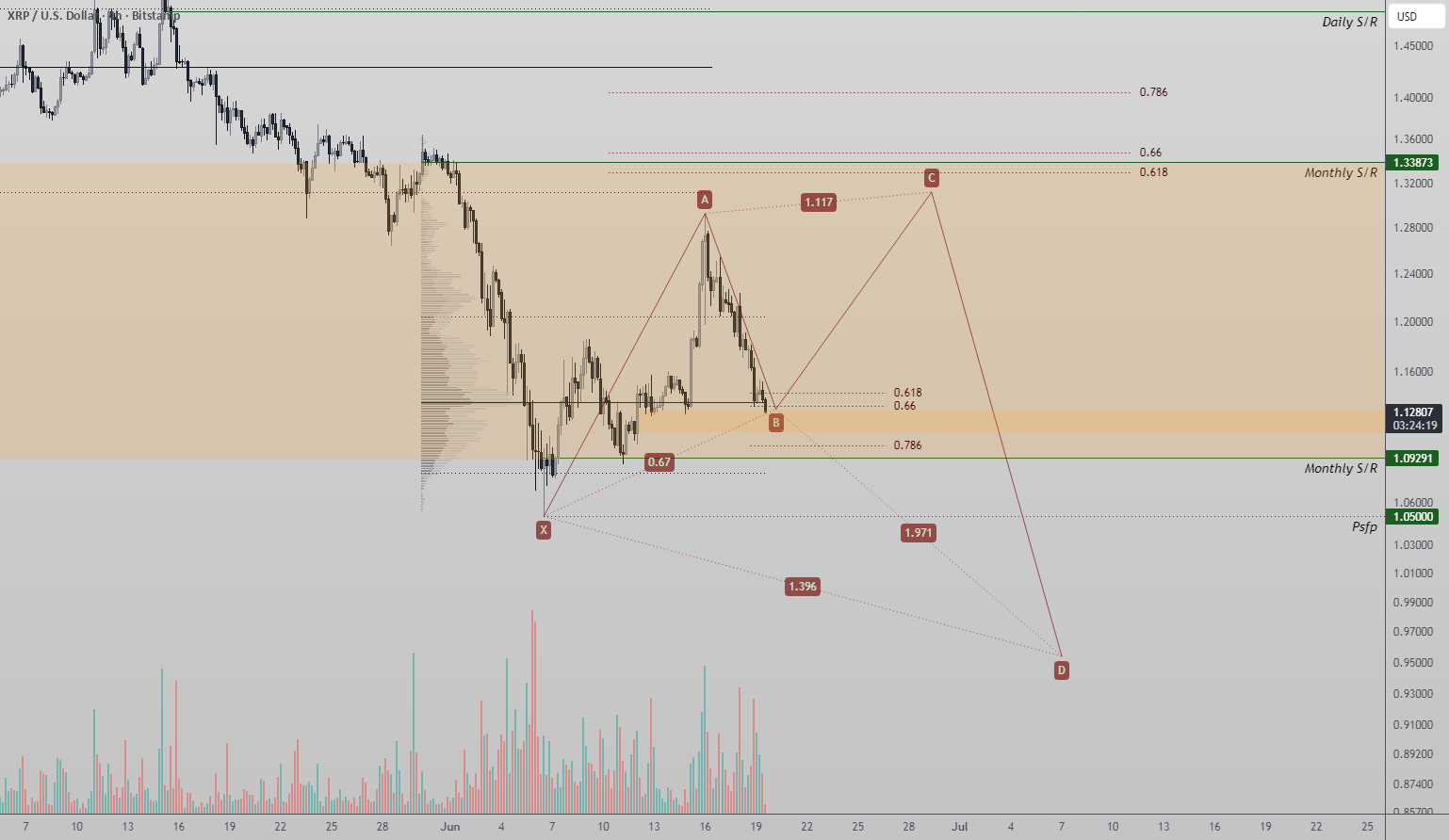

XRP Reversal Setup Forms Around Harmonic Pattern And Key Support Zone

A TradingView analyst says XRP is testing a technically important support zone s...