India’s Food Service Market Is Set for a Breakout: On Track to Cross $125 Billion by 2030

Alex Smith

6 months ago

Synopsis: India’s food-service industry is entering a defining decade, transforming from unorganised eateries into a tech-enabled, organized, and consumption-driven market projected to cross $125 billion by 2030. Led by QSRs, cloud kitchens, and delivery platforms, and powered by rising incomes, Gen Z spending, and digital adoption, India’s food consumption is becoming more convenient, global, healthier, and deeply embedded in everyday life.

India’s food service industry is undergoing a major transformation. What was once a largely unorganised, small-eatery-driven sector is rapidly becoming one of the country’s most dynamic, tech-enabled, and consumption-powered markets.

A recent Swiggy–Kearney report (How India Eats 2025) estimates the market at USD 78 billion in 2025, up from USD 49 billion in 2019, and projects it to cross USD 125 billion by 2030. That’s a massive 60% jump in just five years, marking the beginning of a new era for eating out and ordering in.

Organised Players Take the Lead

One of the most significant shifts underway is the rise of the organized segment: QSR chains, cloud kitchens, dessert parlours, and new-age cafes. Organised share is expected to rise from 45% in 2025 to 55% by 2030 (vs 35-40% in 2019). The organised segment is projected to grow at 12-14%, significantly faster than the 5-7% growth rate for the unorganised segment during the 2025-2030 period. Cloud kitchens (32–37%), QSRs (15–17%), and dessert/ice cream parlours (14–16%) are leading this acceleration.

This organized push is driving better standardization, stronger brands, and more consistent customer experiences, gradually making the market resemble consumption-heavy economies like China and Brazil, where the sector contributes 5% and 6% to GDP, respectively, compared with just 1.9% in India.

Why the Boom? Four Structural Drivers

1. Rising incomes and higher spending power: More households now have the means to eat out or order in frequently, an essential ingredient for category growth. Gen Z will account for more than $1Tn in spending by 2030.

2. Rapid digital adoption: Food delivery and quick commerce have become everyday habits. India’s smartphone penetration is rising toward 70%, and by 2030, nearly 400 million Gen Z and 350M Millennials.

3. A new consumer mindset: Modern Indian consumers, especially urban youth, want convenience, variety, experimentation, and global flavours. Ordering in is no longer a luxury; it’s part of daily life.

4. Massive supply-side expansion: More cloud kitchens, national QSR chains, multi-brand delivery players, premium dessert formats, and café concepts mean more choice, more accessibility, and faster delivery.

How Are India’s Eating Habits Evolving?

The report highlights a dramatic shift in Indian ordering behaviour, with customers exploring 20% more unique cuisines and ordering from 30% more restaurants than before. Healthy, “better-for-you” meals are expanding at 2.3× the overall market, while hyper-regional Indian cuisines such as Goan, Bihari, and Pahari are growing 2–8× faster than mainstream categories. Global flavors are surging as well; Korean cuisine has grown 17×, Vietnamese 6×, and Mexican 3.7× since 2022, alongside rapid rises in beverage trends like buttermilk and sharbat (4–6× growth), boba tea searches (+11×), and matcha tea searches (+4×). Overall, food in India is becoming more global, experimental, and highly personalized. Food in India is becoming richer, more experimental, more global, and more personalized.

Growth Far Beyond Metros

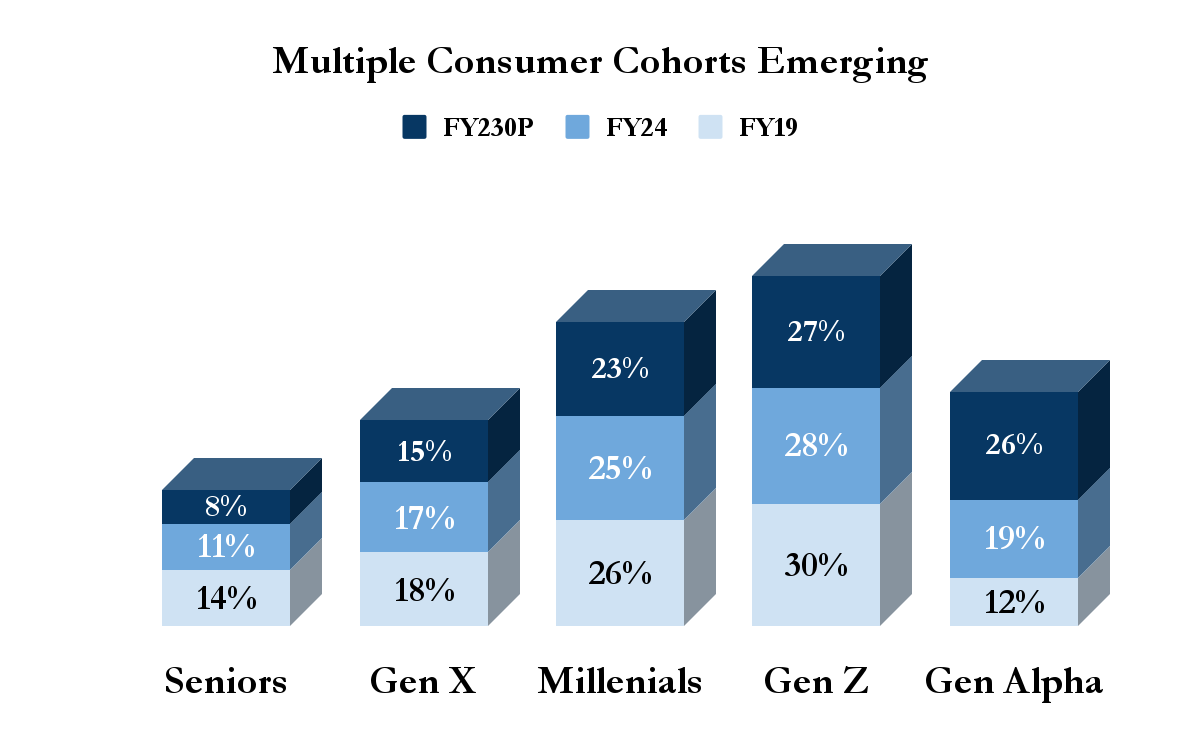

Food-service growth today isn’t limited to Delhi, Mumbai, or Bengaluru. Corporate hubs, educational towns, industrial belts, and tourist centres are emerging as high-growth food markets. Younger consumers (especially Gen Z) are growing 3× faster than other age groups in the dining-out segment, that of dinner, with pizza, cakes and soft drinks witnessing the highest growth in consumption post 11 pm. Restaurants in 700+ cities now offer 24/7 delivery. They also drive demand for innovations: think trendier cafe concepts, “Instagram-worthy” restaurant experiences, and novel menus. India’s food story is now a national story.

A complementary Redseer analysis highlights how India’s broader consumption shift strengthens the food-services boom.

India’s food-services sector is at an inflexion point, powered by a broader nationwide consumption shift. The QSR market has surged from Rs 34,800 crore in 2020 to over Rs 57,000 crore in 2025, supported by the opening of nearly 10,000 new restaurants in 2020 and an expected 20,000 more by 2025. Digital exposure now reaches twice as many people as TV, making food discovery, influencers, and delivery apps central to eating decisions. Dining out has become one of the biggest discretionary spending categories for Gen Z and Millennials, while India’s experience economy is set to exceed $300 billion by 2030. In parallel, organised branded retail is heading toward $730 billion, increasing consumer trust in national chains and cloud-kitchen networks. Urban family spending is also rising sharply, with annual per-child expenditure climbing from Rs 2.5-4.5 lakh in 2020 to Rs 5.6 lakh in 2025 and projected to cross Rs 7-8 lakh by 2030.

A powerful health and protein shift is reshaping the industry, with protein-forward products and snacks expected to reach Rs 36,000 crore by 2030 at 15% CAGR, and four in five Gen Z consumers viewing protein as essential to their daily intake, driving menu innovation across QSRs, cafés, and cloud kitchens. Together, these forces create a once-in-a-decade opportunity across QSRs and multi-brand chains, cloud kitchens and delivery-first formats, regional cuisine brands ready to scale, healthy and protein-led concepts, and youth-focused cafés, dessert bars, and late-night formats. With India’s GDP, digital reach, and young consumer base expanding simultaneously, food services are primed to become one of the decade’s most powerful consumer categories.

{kind=link}

(Source: Redseer Research & Analysis)

Stocks to Watch

Here are the companies that are likely to benefit from India’s rapidly growing food-service market.

- Jubilant FoodWorks Ltd: Jubilant FoodWorks Limited (JFL), founded in 1995, is a leading food-tech company operating 3,480 stores across India, Turkey, Bangladesh, Sri Lanka, Azerbaijan, and Georgia. The Group franchises Domino’s, Popeyes, and Dunkin’ and also owns Hong’s Kitchen in India and COFFY in Turkey.

- Eternal Ltd: Eternal Ltd (formerly Zomato), founded in 2008 as a restaurant discovery platform, has grown into a major player in food delivery and quick commerce in India. Its four key businesses include Zomato (food delivery in 800 cities), Blinkit (10-minute quick commerce in 100 cities), District (going-out services across 800 cities in India & the UAE), and Hyperpure (B2B supplies across 8 Indian cities).

- Swiggy Ltd: Swiggy, founded in 2014, is India’s leading on-demand convenience platform, partnering with 6.9 lakh delivery partners and 2.6 lakh restaurants across 720+ cities. Its services span food delivery, Instamart’s 10-minute grocery delivery in 128 cities, and innovations like Swiggy Dineout, Scenes, Snacc, Toing and Crew.

- Westlife Foodworld Ltd: Westlife Foodworld Limited (formerly Westlife Development Ltd), incorporated in 1982, operates McDonald’s restaurants in West and South India through its subsidiary Hardcastle Restaurants Pvt. Ltd. As the master franchisee of McDonald’s in these regions, the company focuses on expanding and managing its QSR footprint across the country.

- Devyani International Ltd.: Devyani International Limited, incorporated in 1991, is the largest Yum! Brands franchisee in India and operates 2,000+ stores across 280+ cities in India, Nigeria, Nepal, and Thailand. It runs KFC, Pizza Hut, and Taco Bell outlets; is the sole India franchisee for Costa Coffee, Tea Live, New York Fries, and Sanook Kitchen; and owns brands like Biryani By Kilo, Goila Butter Chicken, and Vaango.

- Sapphire Foods India Ltd: Sapphire Foods, incorporated in 2009, is a leading YUM! Brands franchise operator in India and Sri Lanka, backed by major private equity firms and run by a professional management team. As of September 30, 2025, it operates 529 KFC and 338 Pizza Hut restaurants in India, along with 119 Pizza Hut and 11 Taco Bell outlets in Sri Lanka.

- Restaurant Brands Asia Ltd.: Restaurant Brands Asia Limited (RBA), incorporated in 2013, is the national master franchisee for Burger King in India, with exclusive rights to develop and operate the brand nationwide. As of September 30, 2025, it operates 533 stores with 119K average daily sales. Its subsidiaries also serve as the exclusive master franchisees for Burger King and Popeyes in Indonesia.

A One-Line Takeaway for Readers

“India’s food-services market is being rewritten, powered by rising incomes, digital lifestyles, Gen Z spending, and a nationwide appetite for convenience, health, and global flavours. QSRs, cloud kitchens, and experience-led dining are at the heart of this transformation.” With these powerful shifts reshaping how India eats, the nation’s food-services market is firmly on course to achieve, and potentially exceed, the $125-billion mark by 2030.

Written by Shashi Kumar

Disclaimer

The views and investment tips expressed by investment experts/broking houses/rating agencies on tradebrains.in are their own, and not that of the website or its management. Investing in equities poses a risk of financial losses. Investors must therefore exercise due caution while investing or trading in stocks. Trade Brains Technologies Private Limited or the author are not liable for any losses caused as a result of the decision based on this article. Please consult your investment advisor before investing.

The post India’s Food Service Market Is Set for a Breakout: On Track to Cross $125 Billion by 2030 appeared first on Trade Brains.

Related Articles

5 Stocks Recommended by Top Brokerages That Can Deliver Returns of Up to 45%

Synopsis: Five top brokerages have issued fresh Buy calls across IT, FMCG, trave...

₹3,200 Cr Order Book: Can This Smart Meter Stock Evolve Into an Electrical Solutions Co.?

Synopsis: HPL Electric delivered a record FY26, backed by strong smart meter dem...

Tata Motors: Can It Double Passenger Vehicle Volumes and Reach 20% Market Share by FY31?

Synopsis: Tata Motors targets strong PV growth with EV-led expansion, aiming to...

KPIT Technologies: Will Q1 Results Be Strong Enough For A Turnaround?

Synopsis: KPIT Technologies has spent the past year explaining why growth slowed...