Kaynes Tech Shares Have Crashed 60% From Highs But Can It Ever Reach ₹7,700 Again?

Alex Smith

1 month ago

Synopsis: Kaynes Technology was once one of the market’s biggest electronics manufacturing success stories, but the stock has fallen nearly 60 percent from its Rs. 7,700 peak. With accounting concerns, missed expectations and execution challenges on one side, and ambitious growth plans on the other, can the company make a comeback?

Kaynes Technology has gone from being one of the most loved electronics manufacturing stories in India to one of the most debated stocks on Dalal Street. The shares have corrected almost 60 percent from highs of around Rs. 7,700 in October 2025 and are now trading in the range of Rs. 3,000 to Rs. 3,150, forcing investors to ask whether the earlier excitement was justified or whether the stock had simply run too far ahead of execution.

Kaynes Technology India Limited is an integrated Electronics System Design and Manufacturing company. In simple terms, it helps customers design, manufacture, assemble, test and support electronic products. Its products are used across automotive, industrial, EV, aerospace, strategic electronics, railways, medical and IoT segments.

The company has close to four decades of experience and has served more than 500 customers across 30-plus countries, including marquee multinational customers.

Why Did The Stock Crash?

The fall in Kaynes was not because the company suddenly stopped growing. In fact, its FY26 revenue grew 33.2 percent year-on-year to Rs. 3,626.4 crore, while EBITDA rose 39.8 percent to Rs. 574.1 crore and profit after tax increased 24 percent to Rs. 363.9 crore. The order book also expanded to Rs. 8,366.3 crore from Rs. 6,596.9 crore in FY25.

The real problem was that the market had priced Kaynes like a clean high-growth electronics and semiconductor platform, but the company started facing questions around accounting, disclosure quality, working capital, execution delays and guidance credibility. When a stock trades at a premium valuation, even small doubts can lead to a sharp derating. In Kaynes’ case, those doubts came together at the same time.

The company had earlier created high expectations around growth, OSAT, PCB manufacturing, smart meters and product-led revenues. But execution did not keep pace with expectations. Management admitted in the Q4FY26 call that near-term topline performance did not fully meet market expectations due to geopolitical disruption, customer deferments, supply chain delays and product timing shifts. This made investors question whether the order book was converting into revenue as smoothly as expected.

The Kotak Issue: What Was The Real Concern?

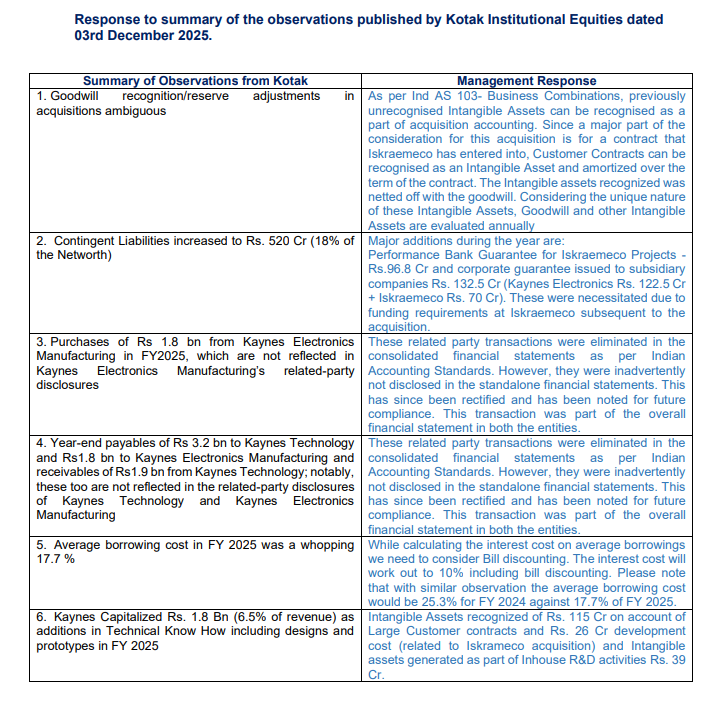

The biggest turning point was the Kotak Institutional Equities report, which flagged concerns around Kaynes’ accounting and disclosure practices. Kotak’s concerns were mainly around the Iskraemeco acquisition, goodwill and intangible asset accounting, contingent liabilities, related-party disclosures, borrowing cost and capitalization of technical know-how.

The most important accounting issue was linked to the Iskraemeco acquisition. Kotak raised concerns that customer contracts were converted into intangible assets and amortized over time under Ind AS 103. While this may be legally permitted, Kotak’s concern was that such treatment can smooth profits and make earnings look less volatile than they actually are. Kaynes responded by saying that since a major part of the acquisition consideration was for customer contracts, those contracts could be recognized as intangible assets and amortized over the contract period.

The second concern was contingent liabilities, which rose to Rs. 520 crore, equal to around 18 percent of net worth. These included performance bank guarantees and corporate guarantees linked to subsidiaries. Kaynes said these guarantees were required for Iskraemeco projects and subsidiary funding needs after the acquisition. The issue here is not that these are current liabilities, but that they represent potential risk if execution or payments do not move as expected.

Kotak also highlighted weak disclosure discipline around Rs. 180 crore of group company purchases and around Rs. 510 crore of inter-group payables and receivables. Kaynes clarified that these transactions were recorded in the financial statements and eliminated in consolidated accounts, but were inadvertently not disclosed in standalone financial statement notes. The company called it a disclosure omission, not an accounting fraud.

Another concern was the average borrowing cost, which appeared to be 17.7 percent. Kaynes responded that the correct calculation should include bill discounting and that the cost would work out to around 10 percent. Kotak also questioned the capitalization of Rs. 180 crore as technical know-how and prototypes, while Kaynes said this included Rs. 115 crore of customer contracts, Rs. 26 crore of acquisition-related development cost and Rs. 39 crore of in-house R&D assets.

{kind=link}

Source: Kaynes Technology India Limited

What Has Changed After The Controversy?

The important thing is that the accounting issue has not become a larger visible crisis so far. Kaynes issued a clarification, held a detailed business update call and responded to major observations. There has been no restatement disclosed in the documents provided, and management has repeatedly said there is no governance concern or underlying business deterioration.

However, the controversy did change the market’s view. Earlier, investors were willing to value Kaynes based on its long-term semiconductor and electronics dream. Now, investors want proof. They want cleaner disclosures, better cash flow, faster order conversion and less aggressive guidance.

In Q3FY26, management said the OSAT facility at Sanand was operational and that approval under the ISM framework had been received. This was important because it improved visibility on capital subsidy and reduced uncertainty around the semiconductor roadmap. Management also said the new HDI multilayer PCB facility in Chennai could create a large business opportunity by combining PCB manufacturing with PCB assembly work from the same customers.

By Q4FY26, the company said OSAT Unit 1 was fully operational and Unit 2 was moving toward commercialization. It also spoke about revenue visibility of more than Rs. 2,500 crore from OSAT over the next five years and a strong confirmed demand pipeline for PCB. These are real positives because they show that Kaynes is not just talking about future businesses; it is actually building the infrastructure.

Where The Business Still Looks Strong

Kaynes’ core business remains attractive. The company is present in high-growth areas such as EV electronics, industrial electronics, aerospace, strategic electronics, railways, medical and IoT. Its revenue mix is also diversified, with industrial including EV contributing the largest share in FY26, followed by automotive and other verticals.

The company is also trying to move up the value chain. Instead of remaining only an EMS assembler, it wants to become an integrated electronics player with EMS, PCB and OSAT capabilities. This is important because PCB gives backward integration, OSAT gives semiconductor exposure and product engineering can improve margins.

Management has also stated that it wants to increase the contribution of new product development and value-added solutions to nearly 30 percent of revenue in the coming years. If this happens, Kaynes may become a more design-led and product-led company rather than just a manufacturing service provider.

Where The Risks Are Still Serious

The biggest risk is working capital. Net working capital days increased from 87 days in FY25 to 125 days in FY26. Inventory days rose from 91 to 97, while receivable days increased from 84 to 134. This means that even though the company is growing, more cash is getting stuck in inventory and receivables.

Management has explained that the smart meter business has a different working capital cycle compared to core EMS. In the Q4 call, it said the core EMS business improved working capital days from 83 days in FY24 to 53 days in FY26. But consolidated numbers still look stretched because smart meters involve installation, government processes and delayed payments.

The second risk is guidance credibility. In Q3, management was still talking about large ambitions, including a billion-dollar revenue scale by FY28, supported by EMS, PCB and OSAT. But after missing earlier expectations, investors will not give full value to future targets unless quarterly execution improves.

The third risk is profitability pressure. In Q4FY26, revenue grew 26.2 percent year-on-year to Rs. 1,242.6 crore, but profit after tax fell 21.5 percent to Rs. 91.2 crore. PAT margin dropped from 11.8 percent to 7.3 percent due to higher depreciation, finance cost and tax expenses. This shows that growth alone is not enough, margins and cash conversion also matter.

Can Kaynes Reach Rs. 7,500 Again?

Kaynes can reach Rs. 7,500 again, but not simply because it traded there earlier. For that to happen, the company must rebuild trust. The first requirement is visible improvement in working capital, especially in smart meters. The second is stronger execution in converting the Rs. 8,366.3 crore order book into revenue. The third is meaningful revenue contribution from OSAT and PCB. The fourth is better disclosure discipline so that accounting concerns do not return.

The long-term story is still alive. Kaynes has the right sectors, a large order book, expanding capabilities, OSAT progress and a PCB opportunity. But the stock’s earlier valuation was based on belief. The next rerating will need proof.

In conclusion, Kaynes is not a broken company, but it is no longer a blind faith stock. At Rs. 7,500, the market valued the dream. At Rs. 3,000 to Rs. 3,150, the market is asking for delivery. If Kaynes fixes working capital, scales OSAT and PCB, improves cash flow and avoids further guidance disappointments, the stock can regain lost ground. But if execution remains patchy, the Rs. 7,500 level will remain a memory rather than a realistic milestone.

Disclaimer: The views and investment tips expressed by investment experts/broking houses/rating agencies on tradebrains.in are their own, and not that of the website or its management. Investing in equities poses a risk of financial losses. Investors must therefore exercise due caution while investing or trading in stocks. Trade Brains Technologies Private Limited or the author are not liable for any losses caused as a result of the decision based on this article. Please consult your investment advisor before investing.

The post Kaynes Tech Shares Have Crashed 60% From Highs But Can It Ever Reach ₹7,700 Again? appeared first on Trade Brains.

Related Articles

Dr. Reddy’s Laboratories: Can It Overcome the Semaglutide Supply Disruption?

Synopsis: Dr. Reddy’s Laboratories faces a temporary semaglutide supply di...

Power Stock Shifting from EPC Projects to a High-Margin Power Services Business to Keep on Your Radar

Synopsis: A power equipment manufacturer has quietly walked away from low-margin...

Pharma Stock That Can Deliver 20% PAT Growth and 24% EBITDA Margin to Add to Your Watchlist

Synopsis: The shares of this pharmaceutical company could deliver 20 percent PAT...

Stocks Under ₹250 with a PEG Ratio Below 1 Trading at a Discount of Up to 52%

SYNOPSIS: Here’s the list of stocks under ₹250 with PEG ratios below 1 and tradi...