What’s driving India’s diagnostic market toward a strong 12% CAGR and a projected $15–16 billion size over the next five years?

Alex Smith

6 months ago

Synopsis: India’s diagnostic market is on a strong growth path, set to expand at 12% CAGR to $15-16 billion over the next five years, driven by rising preventive and wellness testing, ageing demographics, insurance coverage, and expansion into tier-2/3 towns. While pricing pressure and intense competition persist, consolidation, AI adoption, and high-margin segments like genomics are strengthening organised players and shaping the sector for next-phase growth.

The answer lies in the sector’s growing role in preventive and wellness testing, which is rapidly becoming a major demand engine, supported by expanding healthcare infrastructure across tier-2/3/4 towns and broader insurance coverage.

India’s position as one of the most affordable diagnostic markets globally is further accelerating uptake. At the same time, competition from unorganized players and new entrants, from pharma giants to hospital networks, is pushing the industry toward consolidation. With these shifts raising questions about how sustainable the current growth trajectory truly is!!!.

India’s Diagnostics Sector—An Evolving Giant

India’s diagnostic services market is one of the most diverse and fragmented in the world. Most of the country’s 1.3 lakh laboratories are dominated by standalone centres or hospital-based labs, while organized diagnostic chains make up only 20-25% of the market. This fragmentation limits scalability and creates wide variation in service quality. Still, the sector is steadily moving toward consolidation as large players expand their reach.

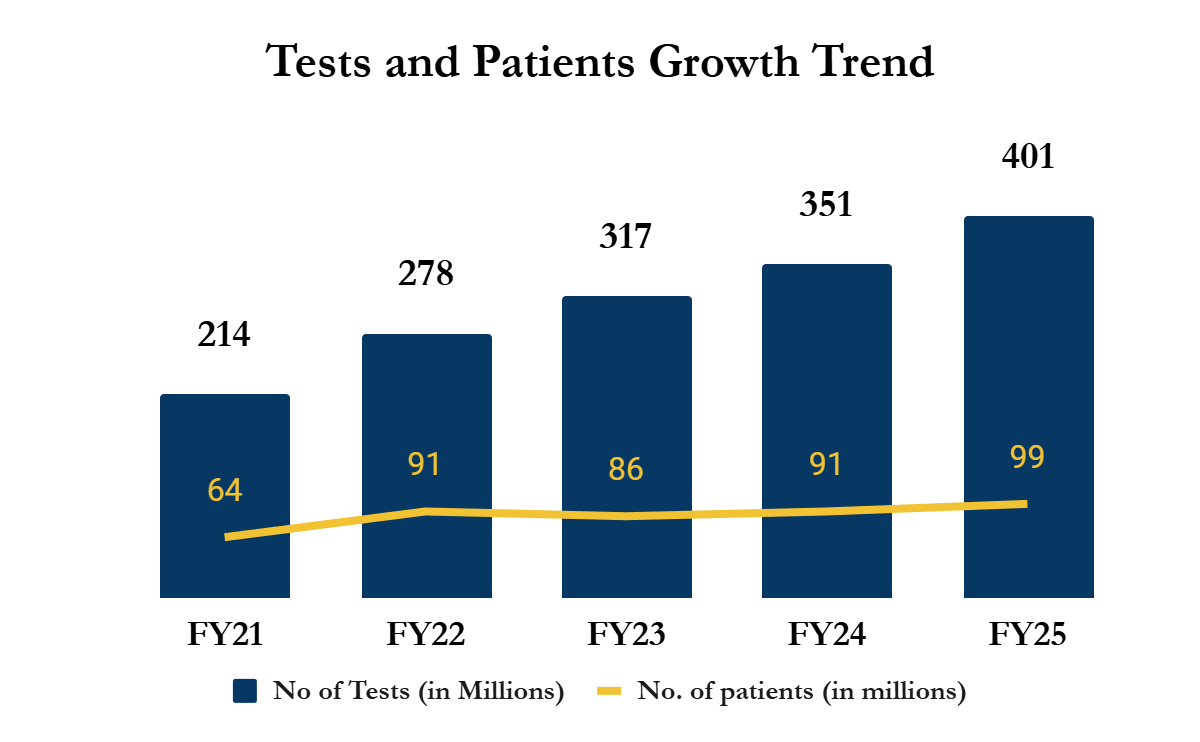

A close look at seven sample diagnostic companies, including Dr Lal Pathlabs, Thyrocare Technologies, Suraksha Diagnostics, Vijaya Diagnostics, Krsnaa Diagnostics, Agilus Diagnostics, and Metropolis Healthcare, which collectively represent about 10-12% of the market, reveals how the industry has grown over the past few years. These players recorded a 12% CAGR in net sales between FY20 and FY25. The pandemic years (FY21 and FY22) saw an extraordinary spike, resulting in a 32% increase in net sales and a corresponding boost in margins to 29-32%, driven by widespread COVID-19 testing. Once pandemic-related demand faded, revenue and profitability returned to normal levels, but the sector’s long-term growth drivers remained strong.

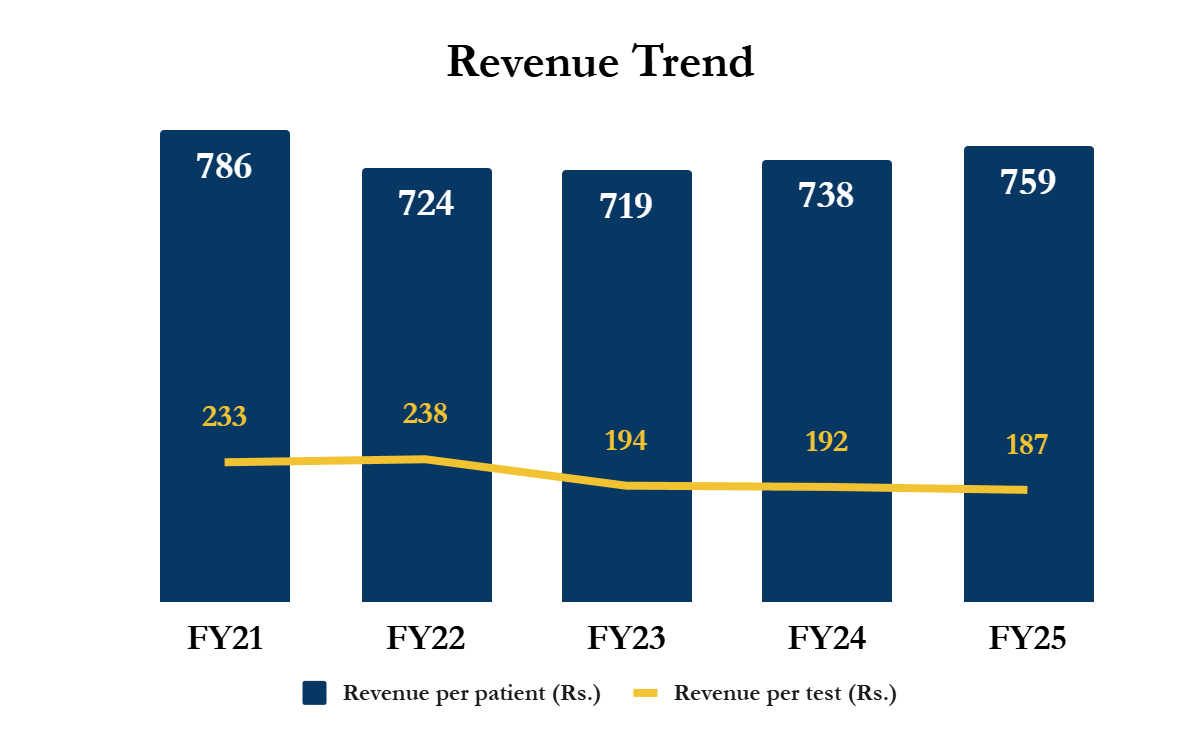

Most of the revenue growth has come from rising volumes. Patient footfall grew at 12% CAGR, while the number of samples collected expanded even faster at 17% CAGR. As big diagnostic chains continue to expand, they are capturing more of this growing demand and helping the industry become more organized. However, competitive pressures have pushed prices downward: revenue per patient fell from Rs 786 in FY21 to Rs 759 in FY25, and revenue per test dropped from Rs 233 to Rs 187 over the same period.

{kind=link}

{kind=link}

Source: CareEdge Report

Key Highlights: Wellness and Preventive Testing in India

Wellness and preventive testing grew at a 25% CAGR between FY21 and FY25. For leading companies, this segment contributed 12-25% of total revenue in FY25, up from 6-12% in FY21. Despite 60%+ of the population being in rural areas, 70%+ of diagnostic revenue comes from cities. Expansion into tier 2-4 towns presents huge growth potential. The South and West hold 58% of NABL-accredited labs; the North and East remain underserved. According to UN projections, India’s population aged 45 years and above is expected to grow by 2.3-2.4% annually between 2020 and 2050, compared to overall population growth of 0.6-0.7%.

Rapidly growing, premium segment with higher margins, supporting disease diagnosis, cancer therapy guidance, and preventive care decisions. Genomic testing is emerging as a significant growth driver for the Indian diagnostic industry. The genomic testing segment consistently delivers double-digit revenue growth, supported by a superior product mix and higher profitability margins.

Challenges: Margin Pressure & Rising Competition

- Highly fragmented market dominated by standalone labs and hospital-based centres.

- Fragmentation limits scalability, investment, and consistent service quality.

- Revenue per patient and per test has marginally declined over five years.

- The entry of pharma companies, hospital chains, and e-pharmacies intensifies competition.

- Pricing per test and margins are expected to remain under pressure.

- Smaller labs face growing margin challenges and limited sustainability.

- High AI adoption costs create barriers for smaller players and also require specialized equipment, skilled scientists, and advanced software, limiting smaller players.

Solutions & Opportunities: Efficiency, Innovation & Consolidation

- Diagnostic chains must rely on volume growth and operational efficiency.

- AI offers faster, more accurate diagnostics and supports preventive care.

- Industry consolidation is accelerating, strengthening organised players.

- Strong investor confidence with six major diagnostic companies listed.

- Private equity investments have surged, highlighted by Neuberg Diagnostics securing Rs 940 crore from Kotak Strategic Situations India Fund II.

- Additionally, a series of smaller acquisitions, each under Rs 50 crore, signals accelerating market consolidation.

Stocks to Watch

- Dr Lal PathLabs Ltd.: Dr. Lal PathLabs is one of India’s leading diagnostic service providers, offering a wide range of tests for diagnosis, monitoring, and disease prevention through its nationwide network. As of March 31, 2025, it operates 298 laboratories, 6,607 patient service centers, and 12,365 pickup points, serving patients, hospitals, and corporate clients.

- Vijaya Diagnostic Centre Ltd: Vijaya Diagnostic Centre is one of India’s largest integrated diagnostic chains, offering both pathology and high-end radiology services through 159 centres and 17 labs with NABL accreditations across 27 cities. It provides a complete one-stop diagnostic solution across key states, including Telangana, Andhra Pradesh, Maharashtra, Karnataka, NCR, and West Bengal.

- Fortis Healthcare Ltd.: Fortis Healthcare Limited is a leading integrated healthcare provider in India, offering hospital, diagnostic, and day-care specialty services. It operates 33 healthcare facilities across 11 states, with 5,800 operational beds and over 400 diagnostic labs.

- Metropolis Healthcare Ltd.: Metropolis Healthcare, established in 1981, is India’s second-largest diagnostic chain, offering high-quality pathology services across India and Africa. With 221 labs, 4,600+ patient service centers, and 10,000+ touchpoints across 28 states and 750+ towns, it serves millions annually with reliable diagnostic insights.

- Thyrocare Technologies Ltd: Thyrocare Technologies is India’s first fully automated diagnostic laboratory chain, offering affordable, quality tests to hospitals and labs nationwide. With 10,000+ active quarterly franchises, it maintains a wide PAN-India network and processed over 53.3 million tests in Q2FY26.

- Krsnaa Diagnostics Ltd.: Krsnaa Diagnostics Ltd., India’s fastest-growing diagnostic services provider in radiology and pathology, started in 2011 with 2 radiology centres and now operates 4,000+ centers across 15 states and 3 Union Territories. The company delivers accurate reports through advanced cloud-based PACS and a global team of radiologists and pathologists, ensuring prompt turnaround and world-class healthcare services.

- Suraksha Diagnostic Ltd.: Suraksha Diagnostic Limited is a leading provider of integrated pathology, radiology, and medical consultation services, offering a seamless experience through a wide operational network. As the largest diagnostic chain in West Bengal, Bihar, Assam, and Meghalaya, the company’s central reference lab is CAP-accredited, 4 labs hold NABL accreditation, and 3 advanced diagnostic centers are NABH-accredited.

Conclusion

Looking ahead, India’s diagnostic market is set to grow at a 12% CAGR, reaching $15-16 billion by FY30, driven by preventive healthcare awareness, demographic shifts, and expanding insurance coverage. With pricing expected to remain stable, volume growth, operational efficiency, and technology adoption (AI, genomic testing) will be key for profitability. Further, PE funding and M&A activity will accelerate this transition.

Written by Shashi Kumar

Disclaimer

The views and investment tips expressed by investment experts/broking houses/rating agencies on tradebrains.in are their own, and not that of the website or its management. Investing in equities poses a risk of financial losses. Investors must therefore exercise due caution while investing or trading in stocks. Trade Brains Technologies Private Limited or the author are not liable for any losses caused as a result of the decision based on this article. Please consult your investment advisor before investing.

The post What’s driving India’s diagnostic market toward a strong 12% CAGR and a projected $15–16 billion size over the next five years? appeared first on Trade Brains.

Related Articles

4 Stocks Riding India’s E-Waste Recycling Boom to Keep on Your Radar

Synopsis:- As stricter Extended Producer Responsibility norms, rising e-waste vo...

5 Stocks Investors Should Look Out for Amid Strong Data Center Demand

Synopsis: India’s data centre industry is entering a phase of unprecedente...

Data Patterns And Other Defence Stocks Capturing High-Margin Electronics Boom

Synopsis: Modern warfare has undergone a fundamental transformation, shifting th...

Railway Stocks: How Kernex, HBL, Quadrant, and RailTel Are Monetizing the Kavach Rollout

Synopsis: As Indian Railways accelerates its Kavach train-protection rollout, a...