Ather Energy receives ‘Buy’ recommendation from Emkay Global; Check the upside

Alex Smith

2 hours ago

Synopsis: Emkay Global has maintained a “buy” rating on Ather Energy, raising its target to ₹1,150, implying ~32% upside, citing strong EV adoption, policy support, and Ather’s premium positioning. The company shows 50% revenue growth, rising volumes, expanding market share, and improving distribution and charging infrastructure.

The shares of a Mid-Cap company specialising in the design, development, manufacturing, and sale of intelligent electric two-wheelers (E2Ws) are in focus following the target by a Brokerage firm Emkay Global with an upside potential of 32 percent.

With a market capitalization of Rs. 33,529.82 crores in the day’s trade, the shares of Ather Energy Ltd rose upto 1.66 percent, making a high of Rs. 886.95 per share compared to its previous closing price of Rs. 872.40 per share.

What Happened

Ather Energy Ltd engaged in the design, development, manufacturing, and sale of intelligent electric two-wheelers (E2Ws), is in the spotlight as Emkay Global has maintained its “buy” rating on Ather Energy, and has raised its price target to Rs. 1,150 from Rs. 1,000 earlier, which implies an upside potential of 31.8 percent from the previous close price.

Reason for the Target

Structural Shift Toward ElectrificationThe transition from internal combustion engine vehicles to electric mobility is expected to be long-term and structural, not cyclical. Similar to the 1990s shift from scooters to motorcycles, EV adoption is gaining momentum due to policy push, cost efficiency, and environmental concerns, creating sustained demand growth.

Rising Fuel Prices Accelerating AdoptionGeopolitical tensions, especially in West Asia, are increasing global fuel price volatility. Higher petrol prices make electric two-wheelers more economically attractive in terms of total cost of ownership. This cost advantage is expected to accelerate EV adoption, directly benefiting players like Ather and TVS.

Strong Product Positioning by AtherAther has positioned itself as a premium electric scooter brand with a strong focus on performance, design, and technology. Its offerings appeal to urban, tech-savvy consumers seeking reliability and innovation, enabling it to command better pricing and build strong brand loyalty in a competitive EV market.

Upward Revision in Volume EstimatesEmkay has increased Ather’s FY27 and FY28 volume projections by 2.6% and 4.6%, respectively, indicating improved confidence in demand visibility. This reflects expectations of faster adoption, better distribution reach, and product acceptance. Higher volumes typically lead to operating leverage, improving margins and supporting higher valuation targets.

Expanding Charging and Ecosystem InfrastructureAther’s investment in fast-charging infrastructure (Ather Grid) enhances user convenience and reduces range anxiety. A well-developed ecosystem strengthens customer confidence in EVs, creates entry barriers for new competitors, and supports long-term scalability, which is critical for sustaining growth and justifying higher stock valuations.

Policy Support and IncentivesGovernment initiatives such as subsidies, tax benefits, and stricter emission norms are encouraging EV adoption in India. These policies reduce upfront costs for consumers and improve affordability, thereby boosting demand. Companies like Ather and TVS stand to benefit significantly from this favourable regulatory environment.

Financials & OthersThe company’s revenue rose by 50 percent from Rs. 635 crores in December 2024 to Rs. 954 crores in December 2025. Meanwhile, Net loss declined from Rs. 198 crores to Rs. 85 crores in the same period.

It sold 68,000 units in Q3 FY26, reflecting strong growth momentum with a 50% year-on-year increase and a 3% quarter-on-quarter rise. This indicates solid demand and sustained expansion compared to both the same period last year and the previous quarter.

There is a steady rise in market share from 7.6% in Q1’25 to 18.8% in Q3’26, indicating strong expansion driven by distribution growth. This reflects a consistent upward trend with accelerating gains in recent quarters.

At the same time, EC count increased from 218 to 600 over the same period, nearly 2.5x growth. The parallel rise in distribution points and market share highlights effective scale-up and improved market penetration

It has strong YoY growth in units, with Q3 FY26 volumes reaching 67,851 units compared to 45,252 units in Q3 FY25, reflecting a 50% increase. Growth momentum remains consistent across quarters, with Q1 and Q2 also showing sharp YoY gains of 97% and 67%, respectively.

Ather Energy is an Indian electric two-wheeler manufacturer focused on designing and producing smart electric scooters. Founded in 2013, the company is known for its premium EV scooters such as the Ather 450 series and Rizta, combining performance, connected features, and software-driven user experience.

The company also operates its own charging network called Ather Grid and has an integrated approach covering design, R&D, and manufacturing in India. It positions itself in the urban mobility segment, competing in the growing electric scooter market with an emphasis on technology, build quality, and ecosystem development.

Disclaimer: The views and investment tips expressed by investment experts/broking houses/rating agencies on tradebrains.in are their own, and not that of the website or its management. Investing in equities poses a risk of financial losses. Investors must therefore exercise due caution while investing or trading in stocks. Trade Brains Technologies Private Limited or the author are not liable for any losses caused as a result of the decision based on this article. Please consult your investment advisor before investing.

The post Ather Energy receives ‘Buy’ recommendation from Emkay Global; Check the upside appeared first on Trade Brains.

Related Articles

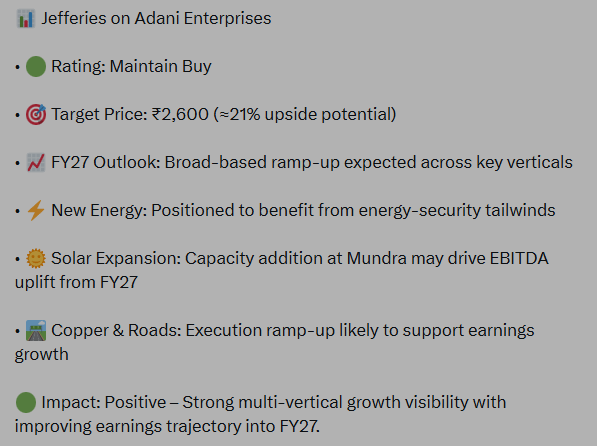

Big Bet by Jefferies: Can Solar Expansion & its Growth Outlook Drive Adani Enterprises Higher?

Synopsis: Jefferies has maintained a Buy rating on Adani Enterprises with a targ...

Amir Chand Exports Stock Soars; Net Profit Jumps 140% in Post-Listing Debut

Synopsis: Amir Chand Jagdish Kumar (Exports) Limited, the miller behind the icon...

ISGEC Heavy Engineering Stock Jumps 3.4% As It Signs MOU with Nigeria for Sugar Plant Development

Synopsis:ISGEC Heavy Engineering signs MOU with Nigeria’s National Sugar D...

NTPC Green Stock In Focus After Commissioning 150 MW Solar Project in Rajasthan

Synopsis: NTPC Green Energy commissions 150 MW Rajasthan solar plant, raising to...