Auto Ancillary Stock Targets 19% Revenue CAGR, Backed by 37 R&D Centres and 11 New Projects

Alex Smith

2 hours ago

Synopsis: A leading auto component maker is strengthening its long-term growth story through product diversification, technology partnerships, expanding EV presence, and rising demand for premium vehicle features across multiple automotive segments.

The shares of this small cap company majorly engaged in manufacturing and supplying of Automotive Solutions and systems to Original Equipment Manufacturers in limelight after the company targets 19 percent revenue CAGR

With the market capitalization of Rs. 66,432 Crores, the shares of Uno Minda Ltd were trading at around Rs. 1150 per share which is 16 percent discount from its 52 week high of Rs. 1382 per share and is trading at a P/E of 54.7 whereas industry P/E stands at 30.1

Premiumisation and EV Shift Drive Higher Component Demand

India’s automobile market is moving towards premium vehicles, with the UV mix rising to 67% in FY26 from 21% in FY16 and the 125cc+ motorcycle mix increasing to 55% from 36%. More features, stricter safety norms and higher EV adoption are increasing component value across vehicles. EVs carry 3-3.5x higher content than ICE models, while Uno Minda’s component value ranges from ₹650-₹20,000 for switches, ₹3,000-₹36,000 for lighting, ₹1,600-₹3,200 for castings and ₹3,400-₹23,000 for seating, positioning it well to benefit from these trends.

LED Adoption Lifts Growth Opportunity in Passenger Vehicle Lighting

The passenger vehicle lighting market is becoming more advanced as LED adoption continues to rise, increasing from around 20% in 2018 to over 30%. SUVs, which now account for 67% of PV volumes in FY26, are driving this trend with wider use of LED headlamps and DRLs. As a result, lighting content per vehicle has nearly doubled from ₹6,000-6,800 in FY20 to around ₹14,200 in FY25 and is expected to reach ₹22,600 by FY30 and ₹37,500 by FY35, supported by technologies such as adaptive LEDs, matrix headlamps, OLED lighting and advanced driver-assistance systems.

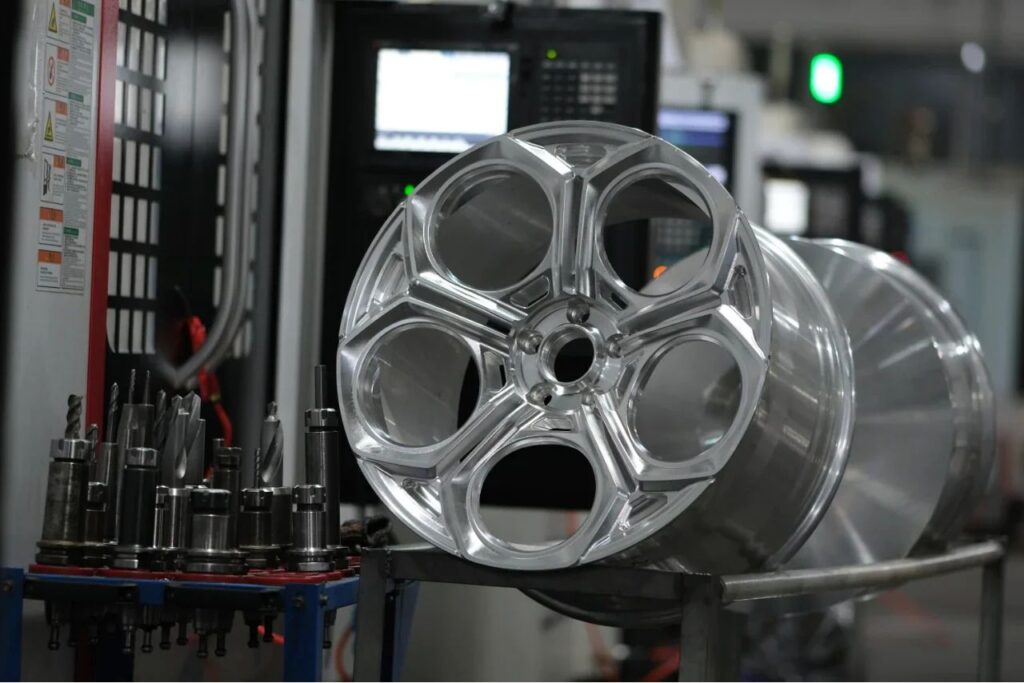

Rising Alloy Wheel Adoption Creates Long-Term Opportunity

The shift from steel wheels to alloy wheels is creating a strong growth opportunity for Uno Minda. In the two-wheeler segment, alloy wheel penetration has reached around 75%, while more than 90% of electric two-wheelers now use alloy wheels to reduce weight and improve driving range.

In passenger vehicles, alloy wheel penetration in India stands at 40-45%, much lower than the 80%+ seen in developed markets, leaving significant room for growth. As SUVs gain popularity and buyers opt for larger alloy wheels, the company expects the addressable market for passenger vehicle alloy wheels to expand by 4 times in the coming years.

Premiumisation and EV Shift Create New Opportunities

The shift towards electric vehicles is creating a major opportunity for Uno Minda, as EVs require far more electronic components than traditional ICE vehicles. Compared with conventional vehicles, EVs use more controllers, sensors, electronic modules, power interfaces and LED lighting, increasing the company’s content per vehicle.

In India, electric two-wheeler sales crossed around 1.4 million units in FY26, with penetration reaching 6.4%. According to Kearney, this is expected to rise to 30% by 2030, taking annual e-2W sales to around 7 million units, nearly 6 times current levels. This could increase Uno Minda’s kit value from around ₹12,000 in ICE vehicles to ₹35,000-40,000 in EVs, implying nearly a 3x rise in content per vehicle.

Margins Expected to Stay Stable Despite Near-Term Cost Pressures

Uno Minda is likely to face higher input and employee costs, along with start-up expenses from around 10 new plants under ramp-up. Despite these pressures, management expects operating margins to remain stable at 11.0-11.5%, supported by a better product mix and its ability to pass on higher costs to OEMs.

The brokerage expects a 50 basis point margin impact in FY27 before margins recover to 11.7% in FY28. The company has planned ₹17 billion capex in FY27 after investing ₹15 billion in FY26 and is expected to deliver a 23% earnings CAGR over FY26-28 while remaining free cash flow positive.

Conclusion:

Uno Minda continues to strengthen its long-term growth story through product diversification, technology partnerships, expanding EV capabilities and a strong R&D base. The company is well positioned to benefit from rising premiumisation, higher content per vehicle and increasing electric vehicle adoption. Despite near-term cost pressures and heavy capital expenditure, stable margins, healthy cash flows and multiple capacity additions provide confidence in its ability to deliver sustained earnings growth over the coming years.

Disclaimer: The views and investment tips expressed by investment experts/broking houses/rating agencies on tradebrains.in are their own, and not that of the website or its management. Investing in equities poses a risk of financial losses. Investors must therefore exercise due caution while investing or trading in stocks. Trade Brains Technologies Private Limited or the author are not liable for any losses caused as a result of the decision based on this article. Please consult your investment advisor before investing.

The post Auto Ancillary Stock Targets 19% Revenue CAGR, Backed by 37 R&D Centres and 11 New Projects appeared first on Trade Brains.

Related Articles

Power Stock Shifting from EPC Projects to a High-Margin Power Services Business to Keep on Your Radar

Synopsis: A power equipment manufacturer has quietly walked away from low-margin...

Pharma Stock That Can Deliver 20% PAT Growth and 24% EBITDA Margin to Add to Your Watchlist

Synopsis: The shares of this pharmaceutical company could deliver 20 percent PAT...

Stocks Under ₹250 with a PEG Ratio Below 1 Trading at a Discount of Up to 52%

SYNOPSIS: Here’s the list of stocks under ₹250 with PEG ratios below 1 and tradi...

Caliber Mining IPO: From Issue Details to Financials; Here’s What You Need to Know

Synopsis: Caliber Mining & Logistics Limited’s ₹450 crore IPO opens on...