Is The AI Bubble Ready To Burst: What Can We Decode From NVIDIA’s Q4 Earnings?

Alex Smith

3 hours ago

Synopsis: NVIDIA’s latest results offer important signals about the strength of the AI boom. While growth remains powerful and demand appears intact, deeper details around spending, supply and financial structures raise bigger questions. The numbers suggest momentum continues, but whether this cycle stays sustainable is the real debate.

The latest quarterly results from the company at the center of the AI boom, Nvidia, have once again raised a big question in global markets: Is artificial intelligence still in a strong growth phase, or are we getting close to a bubble? The numbers look powerful on the surface, but they also reveal important details about demand, supply limits, big tech spending and how money is flowing through the AI ecosystem. These signals may help investors understand whether this rally is built on real business growth or rising financial excitement.

Revenue & Profitability

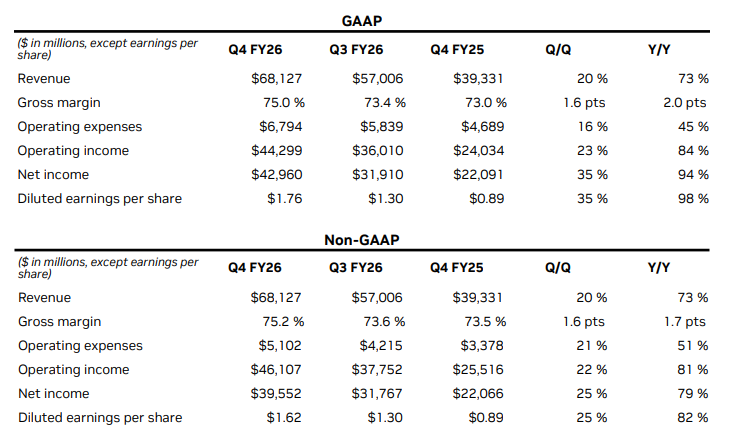

The company reported fourth-quarter revenue of USD 68.1 billion, marking a 73 percent increase year-on-year and a 20 percent rise sequentially. For the full fiscal year, revenue reached a record USD 215.9 billion, up 65 percent compared to the previous year. GAAP net income stood at USD 42.9 billion, up from USD 31.9 billion in Q3FY26, and Non-GAAP net income stood at USD 39.5 billion compared to USD 31.7 billion in Q3FY26.

{kind=link}

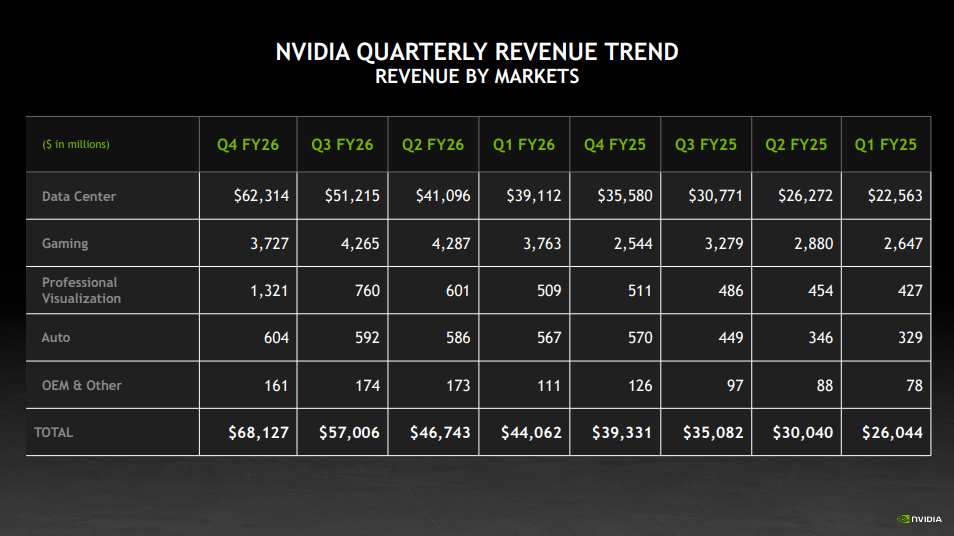

The Data Center business remained the core growth engine. Fourth-quarter Data Center revenue stood at USD 62.3 billion, up 75 percent year-on-year and 22 percent sequentially. For the full year, Data Center revenue rose 68 percent to a record USD 193.7 billion. Hyperscalers continued to be the largest customer segment, contributing slightly over 50 percent of Data Center revenue, although growth during the quarter was driven more by the rest of the customer base as revenue diversified.

Within the Data Center, compute revenue reached USD 51.3 billion, growing 58 percent year-on-year and 19 percent sequentially. Networking revenue surged to USD 11.0 billion, up 263 percent year-on-year and 34 percent sequentially, supported by the ramp-up of NVLink compute fabric for GB200 and GB300 systems along with growth in Ethernet and InfiniBand platforms.

Gaming revenue came in at USD 3.7 billion for the quarter, increasing 47 percent year-on-year due to strong Blackwell demand but declining 13 percent sequentially as channel inventory normalized after the holiday season. Full-year Gaming revenue rose 41 percent to a record USD 16.0 billion. The company indicated that supply constraints are expected to weigh on Gaming in the first quarter of fiscal 2027 and potentially beyond.

Professional Visualization revenue reached USD 1.3 billion in the fourth quarter, up 159 percent year-on-year and 74 percent sequentially, driven by strong Blackwell demand. Full-year revenue for this segment grew 70 percent to a record USD 3.2 billion.

Automotive revenue was USD 604 million in the fourth quarter, increasing 6 percent year-on-year and 2 percent sequentially, supported by continued adoption of its self-driving platforms. For the full year, Automotive revenue rose 39 percent to a record USD 2.3 billion.

Balance Sheet and Liquidity

Cash, cash equivalents and marketable securities stood at USD 62.6 billion at the end of the quarter, up from USD 43.2 billion a year earlier and USD 60.6 billion in the previous quarter. The increase reflects strong revenue growth, partly offset by payments for an intellectual property license, strategic investments and share repurchases.

Accounts receivable totaled USD 38.5 billion, with days sales outstanding improving to 51 days from 53 days in the previous quarter due to the timing of collections. Inventory rose sequentially to USD 21.4 billion from USD 19.8 billion. Total supply-related commitments stood at USD 95.2 billion, indicating secured inventory and capacity to meet demand for several quarters ahead.

Multi-year cloud service agreements increased to USD 27.0 billion from USD 26.0 billion sequentially, supporting expanding research and development requirements.

Cash Flow and Shareholder Returns

Cash flow from operating activities reached USD 36.2 billion in the fourth quarter, more than doubling from USD 16.6 billion a year ago and rising from USD 23.8 billion in the prior quarter, driven by revenue growth.

During the quarter, USD 4.1 billion was returned to shareholders through USD 3.8 billion in share repurchases and USD 243 million in dividends. For fiscal 2026, total capital returned to shareholders amounted to USD 41.1 billion, including USD 40.1 billion in buybacks and USD 974 million in dividends.

{kind=link}

Key Highlights From The Quarter

Data Center

The company introduced the Rubin platform with six new chips aimed at reducing inference token costs by up to 10 times compared with Blackwell. Major cloud providers, including Amazon Web Services, Google Cloud, Microsoft Azure and Oracle Cloud Infrastructure will be early adopters. It also launched BlueField-4 to power a new AI-native storage platform and announced a multiyear partnership with Meta covering CPUs, networking and large-scale Blackwell and Rubin GPU deployments.

Blackwell Ultra was reported to deliver up to 50 times better performance and 35 times lower cost for agentic AI versus Hopper. Partnerships expanded across the ecosystem, including collaborations with Anthropic, Groq and CoreWeave. The company also unveiled Nemotron 3 open models, expanded BioNeMo, joined the U.S. Department of Energy’s Genesis Mission, launched Earth-2 AI weather models and deepened engagements across India’s IT majors and global industrial software leaders.

Gaming and AI PC

The company introduced DLSS 4.5, enhancing AI-driven graphics quality, and launched G-SYNC Pulsar to improve motion clarity for competitive gaming. It also advanced RTX AI capabilities across PCs.

AI performance improvements included up to 35 percent faster large language model inference on AI PCs and up to three times better performance in AI-generated visuals, strengthening its position in AI-enabled personal computing.

Professional Visualization

The RTX PRO 5000 72GB Blackwell GPU was launched to support larger models and complex agent-based workflows.

Global availability of DGX Spark was expanded to support the latest open models, alongside performance upgrades aimed at enterprise and research workloads.

Automotive and Robotics

The company introduced the Alpamayo open AI model family to support safer autonomous vehicle development. It partnered with Mercedes-Benz for enhanced driver assistance in the new CLA and expanded the DRIVE Hyperion ecosystem with major automotive and sensor partners including Bosch and ZF Group.

It also unveiled Cosmos and Isaac GR00T models for robotics, with companies such as Boston Dynamics and Caterpillar adopting its robotics stack. Strategic partnerships were expanded with Siemens and Dassault Systèmes to build industrial AI platforms and digital twin solutions.

Earnings Call Highlights

Data Center Scale And Forward Growth

Management highlighted that the Data Center business has expanded nearly 13 times since the emergence of ChatGPT in fiscal 2023, underlining how central AI has become to the company’s growth story. Looking ahead, they expect sequential revenue growth throughout calendar 2026, surpassing what was previously outlined under the USD 500 billion Blackwell and Rubin revenue opportunity shared last year.

The company has already shipped initial Vera Rubin samples to customers and remains on track to begin production shipments in the second half of the year. Management expects every major cloud model builder to deploy Rubin, reinforcing confidence in continued demand across the next product cycle.

Demand Visibility, Supply Commitments And Power Constraints

Executives stated that inventory and long-term supply commitments are in place to support demand extending into calendar 2027. Inventory rose 8 percent quarter-on-quarter, while purchase commitments increased significantly. The company has secured capacity further out than usual, reflecting stronger demand visibility than in past cycles.

They emphasized that most modern data centers are power-constrained. As a result, customers are making architectural decisions based on performance per watt to maximize AI factory revenues. Despite tight supply for advanced architectures, management expressed confidence in leveraging scale and long-standing supply chain partnerships to meet future growth. Notably, even older Hopper and six-year-old Ampere products are sold out in the cloud, indicating persistent demand across product generations.

Software Optimization And Cost Leadership

Continuous improvements in CUDA software delivered up to five times better performance on GB200 and NVL72 systems within just four months. Management stressed that the company delivers the lowest cost per token in the industry, and data centers built on its infrastructure generate the highest revenues.

With an annual R&D budget nearing USD 20 billion and deep co-design capabilities across chips, systems, networking, algorithms and software, the company aims to deliver step-change improvements in performance per watt with every generation and maintain long-term leadership.

Networking And Mellanox Integration

For the full year, networking revenue crossed USD 31 billion, more than ten times higher than fiscal 2021, the year Mellanox was acquired. This reflects the growing importance of high-speed interconnects and networking in large-scale AI infrastructure.

Hyperscaler CapEx And ROI Signals

Management pointed to strong evidence of return on investment as hyperscalers shift traditional workloads such as search, advertising and recommendation systems toward generative AI. This success is encouraging large customers to accelerate capital spending.

Analyst expectations for 2026 capital expenditure among the top five cloud providers and hyperscalers, which together account for slightly over 50 percent of Data Center revenue, have risen by nearly USD 120 billion since the start of the year and are now approaching USD 700 billion.

On the outlook beyond fiscal 2027, CEO Jensen Huang expressed confidence that hyperscaler cash flows will continue to grow. He argued that the rise of agentic AI marks an inflection point, where compute directly translates into revenue generation. In his words, in the new AI economy, “compute equals revenues,” as tokens cannot be generated without computing capacity. He emphasized that productive and profitable tokens are now being generated for both enterprises and cloud providers, supporting sustained infrastructure investment.

Sovereign AI Expansion

The sovereign AI business more than tripled year-on-year in fiscal 2026 to over USD 30 billion. Growth was driven by customers in Canada, France, the Netherlands, Singapore and the UK. Over time, management expects sovereign AI spending to grow at least in line with the broader AI infrastructure market, with countries investing in AI proportional to their GDP.

China Exposure And Competitive Risks

Management noted that only small volumes of H200 products for China-based customers have been approved by the U.S. government, and no revenue has yet been generated. Future approvals remain uncertain. At the same time, domestic Chinese competitors, strengthened by recent IPOs, are advancing and could influence the long-term structure of the global AI industry. Management stressed that sustained U.S. leadership in AI compute requires broad developer engagement worldwide.

Gaming Outlook

While overall end demand remains strong and channel inventory levels are healthy, the company expects supply constraints to act as a headwind for Gaming in the first quarter and potentially beyond.

Robotics And Autonomous Vehicles

Management highlighted exponential growth in robotaxi rides. Commercial fleets from companies such as Waymo, Tesla, Uber, WeRide and Zoox are expected to scale from thousands of vehicles in 2025 to millions over the next decade. This could create a market generating hundreds of billions of dollars in revenue and require significantly higher levels of compute, with major automotive manufacturers and service providers building on the company’s platform.

Free Cash Flow And Capital Allocation

The company generated USD 35 billion in free cash flow in the fourth quarter and USD 97 billion for fiscal 2026. When asked about accelerating share repurchases given muted stock price movement, CFO Colette Kress stated that capital allocation decisions are made carefully.

She emphasized that supporting the broader ecosystem, including suppliers and early AI developers, remains a priority to ensure adequate supply and platform adoption. While the company continues share buybacks and dividends, it also intends to pursue strategic investments that strengthen long-term growth opportunities rather than focusing solely on aggressive repurchase programs.

Guidance

Starting from the first quarter of fiscal 2027, the company will begin including stock-based compensation expenses in its non-GAAP financial metrics. Management described stock-based compensation as a core part of its pay structure, designed to attract and retain top talent, and believes including it will provide a clearer financial picture.

For the first quarter of fiscal 2027, revenue is projected to be around USD 78.0 billion, with a possible variation of plus or minus 2 percent. Importantly, this outlook does not assume any Data Center compute revenue from China.

GAAP gross margin is expected to be about 74.9 percent, while non-GAAP gross margin is projected at 75.0 percent, both with a margin of error of plus or minus 50 basis points. These figures include an estimated 0.1 percent impact from stock-based compensation.

GAAP operating expenses are expected to be approximately USD 7.7 billion, and non-GAAP operating expenses are estimated at about USD 7.5 billion. These figures include roughly USD 1.9 billion related to stock-based compensation.

For the full fiscal year 2027, the company expects its GAAP and non-GAAP effective tax rate to fall between 17 percent and 19 percent. This estimate excludes any one-time items or significant changes in the tax environment.

Is The AI Bubble Going To Burst?

The fourth-quarter results gave more than just strong revenue numbers. They offered important clues about the state of the AI boom. Since NVIDIA sits at the centre of the AI trade and is the key supplier powering most large AI data centers, its numbers act as a reality check for the entire ecosystem. By looking closely at demand trends, supply commitments, hyperscaler spending and management commentary, we get a clearer picture of whether the current AI cycle is overheating or still backed by real fundamentals. The answer depends on two big forces, real-world limits and financial behaviour.

On one side, supply is still tight. NVIDIA has secured more than USD 95 billion in long-term supply commitments and locked in production capacity well into 2027. Its most advanced chips remain in high demand, and even older Hopper and Ampere chips are sold out in cloud data centers. Many AI facilities are now limited not just by chips, but by electricity and cooling capacity. Even if hyperscalers like Microsoft, Amazon, Alphabet and Meta Platforms wanted to expand much faster, they cannot do it overnight. Advanced chip manufacturing takes time. Packaging and memory supply are limited. Power infrastructure takes years to build. These physical limits slow down reckless expansion. From this view, the AI cycle looks strong but controlled.

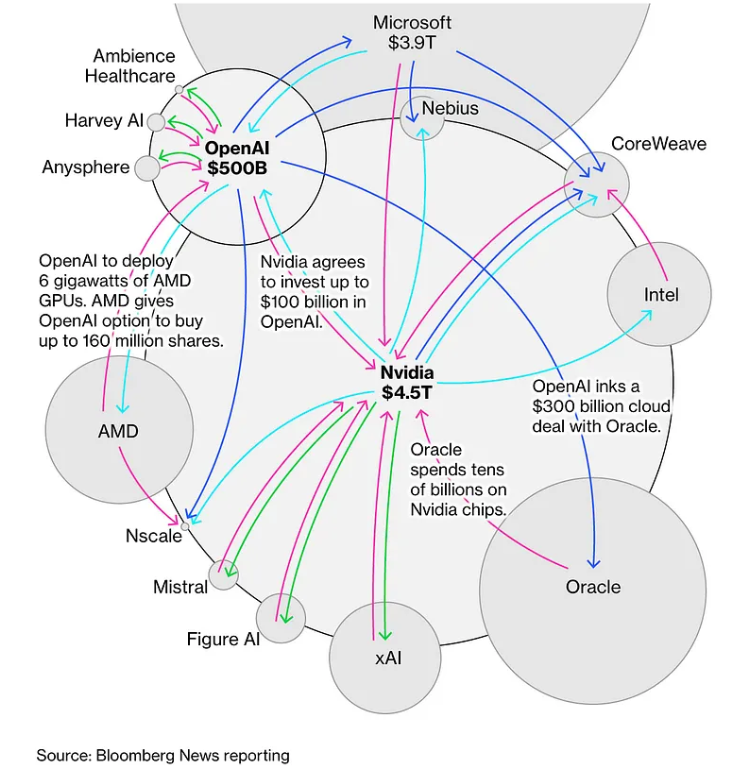

But there is another side to the story. The AI ecosystem is becoming financially connected in new ways. In September 2025, NVIDIA announced plans to invest up to USD 100 billion in OpenAI, linked to 10 gigawatts of compute capacity. That plan was later reduced to a USD 30 billion equity investment after concerns about how the deal might look. Around the same time, OpenAI signed a large agreement with Advanced Micro Devices that included chip purchases tied to equity warrants. Just days ago, Meta announced a similar USD 60 billion deal with AMD that also includes warrants linked to future stock price targets. These types of “equity-for-compute” deals raise questions. Are companies buying chips purely because of real demand, or are financial arrangements helping to drive orders?

There are also challenges in turning big announcements into real infrastructure. The widely discussed USD 500 billion Stargate project involving Oracle, SoftBank Group and OpenAI has reportedly slowed due to internal disagreements and operational issues. Building 10 gigawatts of AI data centers is not just about signing checks. It requires land, power grids, permits and years of construction. Big numbers on paper do not always translate into immediate capacity.

At the same time, hyperscaler AI spending remains massive. By early 2026, Microsoft, Amazon, Alphabet and Meta together are committing close to USD 470 billion a year toward AI infrastructure. As long as these companies are generating real revenue from AI services, advertising improvements and cloud workloads, spending can continue. NVIDIA’s leadership believes that AI compute directly drives revenue, which supports ongoing investment.

So will the AI bubble burst? Right now, there is no clear sign of demand collapsing. Supply remains tight, chips are sold out and capacity is mostly pre-committed. That reduces the risk of a sudden crash caused by oversupply. However, the growing use of equity-linked deals and heavy capital spending means the system depends on continued strong returns. If AI revenues slow or investors lose confidence, spending could quickly cool down.

The AI boom today stands between strong real demand and rising financial complexity. It will not burst simply because too many chips are produced. It would burst only if the money being invested stops generating the returns that justify it.

{kind=link}

Disclaimer: The views and investment tips expressed by investment experts/broking houses/rating agencies on tradebrains.in are their own, and not that of the website or its management. Investing in equities poses a risk of financial losses. Investors must therefore exercise due caution while investing or trading in stocks. Trade Brains Technologies Private Limited or the author are not liable for any losses caused as a result of the decision based on this article. Please consult your investment advisor before investing.

The post Is The AI Bubble Ready To Burst: What Can We Decode From NVIDIA’s Q4 Earnings? appeared first on Trade Brains.

Related Articles

EV Stocks: How Did Olectra Greentech, Ather Energy and Others Perform in Q3?

SYNOPSIS: India’s EV sector continues rapid expansion, but Q3 FY26 results show...

Max vs Fortis vs Apollo: Who Really Leads India’s Hospital Sector?

Synopsis: India’s hospital sector is rapidly expanding, driven by rising demand...

Clean Max Enviro and 4 Other Companies Set to List; Check Listing Date and Other Details

Synopsis: Five IPOs, Omnitech Engineering, PNGS Reva Diamond Jewellery, Shree Ra...

Hidden Gem: Transformer Oil Manufacturing Stock to Keep on Your Radar

SYNOPSIS: This debt-free company and a leading transformer oil manufacturer, rep...