₹20,000 Cr Order book and 36% ROCE : Why This Defence PSU Stock Deserves a Second Look

Alex Smith

1 month ago

Hidden behind larger names is a company quietly powering the Navy, exporting warships, and delivering some of the highest returns in the sector. Let’s deep dive into understanding why Garden Reach Shipbuilders & Engineers stands out as one of India’s most strategically important, yet often underestimated, defence stories.

Industry Overview:

India’s shipbuilding industry is entering a strong multi-year growth phase driven by defence, commercial shipping, and policy support. Defence shipbuilding alone presents an opportunity of over Rs 1.5 lakh crore over the next decade, with the Indian Navy and Coast Guard planning fleets of about 200 ships each and expected to order more than 150 warships over the next 15 years. Commercial shipbuilding adds another Rs 12,000-15,000 crore opportunity annually, led by coastal shipping, dredgers, ferries, cruises and gas carriers.

Under the Maritime India Vision 2030 (MIV 2030), operational national waterways are set to expand from 16 to 23, cargo movement is projected to rise from 73 million tonnes to over 200 million tonnes annually, and ferry passenger traffic is expected to increase fivefold from 14 crore to 70 crore by 2030. To meet these targets and the Sagarmala programme’s goals, India’s coastal and inland waterways fleet will need to triple over the next decade, creating demand of about 12.75 million CGT, along with new opportunities from the push towards green shipping. India’s shipbuilding sector is witnessing a sharp acceleration in growth. From a modest valuation of US$ 90 million in 2022, the industry is set to expand at an extraordinary 60% compound annual growth rate, propelling it to nearly US$ 8,120 billion by 2033, according to Finextra Research.

About Garden Reach Shipbuilders & Engineers Ltd:

Garden Reach Shipbuilders & Engineers Ltd. (GRSE) is a leading Defence Public Sector Undertaking under the Ministry of Defence, with a legacy dating back to 1884 when it began as a small workshop repairing river vessels. The company was formally incorporated in 1934 and later taken over by the Government of India in 1960. GRSE went on to make history in 1961 by becoming the first shipyard of independent India to build a warship for the Indian Navy, the Seaward Defence Boat (SDB) INS Ajay. Over the decades, it has also emerged as a global exporter, built India’s first-ever export warship, “CGS Barracuda” for Mauritius, a Fast Patrol Vessel, “SCG PS Zoroaster” for Seychelles and an Ocean-Going Cargo & Passenger Ferry Vessel, “MV Ma Lisha” for the Cooperative Republic of Guyana. GRSE is the only Indian Shipbuilder to have four distinct shipyards as a unique infrastructure advantage.

So far, GRSE has delivered over 800 platforms, including 114 warships, the highest number built by any Indian shipyard for the Indian Navy, Indian Coast Guard, and friendly foreign nations. Its wide portfolio spans frigates, corvettes, patrol vessels, landing ships, survey vessels, and fast attack craft, along with ship repair. Beyond shipbuilding, GRSE has diversified into engineering, producing prefabricated steel bridges, deck machinery, marine diesel engine overhauls, and 30 mm naval surface guns. Backed by modernized infrastructure, the ability to build 28 ships simultaneously, and strong in-house design capabilities using advanced software and VR labs.

Business Divisions:

- Shipbuilding: The company has delivered around 800 platforms, including 114 warships, the highest by any Indian shipyard, ranging from 5-tonne boats to a 24,600-tonne fleet tanker, and has also supplied vessels to Mauritius and Seychelles. With strong in-house design and construction capabilities, GRSE has played a key role in India’s indigenous warship programme, building complex platforms such as frigates, corvettes, tankers, landing ships, and patrol vessels. The shipyard is now expanding into future technologies, including zero-emission vessels and unmanned and autonomous systems, with India’s largest, with 13 green ferries already in operation and more under construction.

- Ship Repair: GRSE has established a dedicated Ship Repair Division to tap opportunities in both the commercial and defence repair segments. To significantly scale up its ship repair and refit capabilities, the company signed a Concession Agreement with Syama Prasad Mookerjee Port, Kolkata (SMPK) for the development and utilisation of three existing dry docks at the Khidderpore Dry Dock (KPDD) complex in Kolkata. In addition, GRSE is in the process of taking over one more dry dock from SMPK, further strengthening its infrastructure and providing a major impetus to the ship repair business.

- Engineering Business: Beyond shipbuilding and ship repair, GRSE has diversified into the engineering domain. Its engineering portfolio includes prefabricated steel bridges across various spans and configurations, as well as a range of deck machinery such as anchor capstans, boat davits and related equipment. In addition, the Engine Division undertakes the assembly, testing and overhauling of marine diesel engines, along with the manufacture of diesel alternators.

- Weapons: GRSE has further diversified into the weapons segment. It is currently executing an order for 30 mm Naval Guns in collaboration with an Indian firm, with technical support from a reputed foreign partner. The first gun has already been successfully delivered to the Indian Navy after undergoing extensive testing and trials.

Competitive Advantages

- GRSE has delivered over 114 warships to the Indian Navy and Indian Coast Guard and holds the distinction of being the first Indian company to export warships internationally.

- GRSE generates industry-leading returns on capital employed of 36.26% compared to large companies like Cochin Shipyard and Mazagon Dock. With a net debt-to-equity ratio of 0.01 and has better FII holdings than peers with 3.26%.

- GRSE’s order book stands at Rs 20,205.56 crores, making up 76% of market capitalization.

- GRSE uses a robust e-procurement and e-auction system.

- Long-standing relationships with main customers like the Indian Navy and the Indian Coast Guard.

- Proven capability to produce a wide spectrum of ships ranging from 5-tonne boats to 24600-tonne fleet tankers.

Financial Highlights of Garden Reach Shipbuilders & Engineers Ltd

Financial Year2020 (Mar)2021 (Mar)2022 (Mar)2023 (Mar)2024 (Mar)2025 (Mar)5-year CAGRRevenue (Crores)1,4331,1411,7542,5613,5935,07628.78%Net Profit (Crores)16315319022835752726.45%Operating Profit Margin (%)3%7%8%6%7%8%–Return on Capital Employed (%)21.52%18.00%20.33%21.81%29.17%34.19%–Earnings per share (₹)14.2713.416.5519.9131.1946.0426.40%Revenue from operations surged from Rs 1,433 crore to Rs 5,076 crore, translating into a 5-year CAGR of 28.78%, driven by rising execution scale and order inflows. Net profit grew at a healthy 26.45% CAGR, reaching Rs 527 crore in FY25, reflecting improved operating leverage. Profitability and returns strengthened meaningfully. Operating margins remained stable in the 6-8% range, while ROCE improved sharply from 22% in FY20 to over 34% in FY25, indicating efficient capital deployment. EPS more than tripled over five years to Rs 46.04, underlining sustained value creation for shareholders.

For the first half of FY26, the company delivered a strong financial performance across all key metrics. Total income rose to Rs 3,128 crore, up from Rs 2,311 crore in H1 FY25, reflecting a healthy growth of 35%. Revenue from operations increased even faster, climbing 38% year-on-year to Rs 2,987 crore compared with Rs 2,163 crore in the corresponding period last year. Operating profitability also improved significantly, with EBITDA rising 49% to Rs 409 crore in H1 FY26 from Rs 274 crore in H1 FY25. This translated into robust bottom-line growth, as profit after tax (PAT) surged 48% year-on-year to Rs 274 crore against Rs 185 crore in H1 FY25.

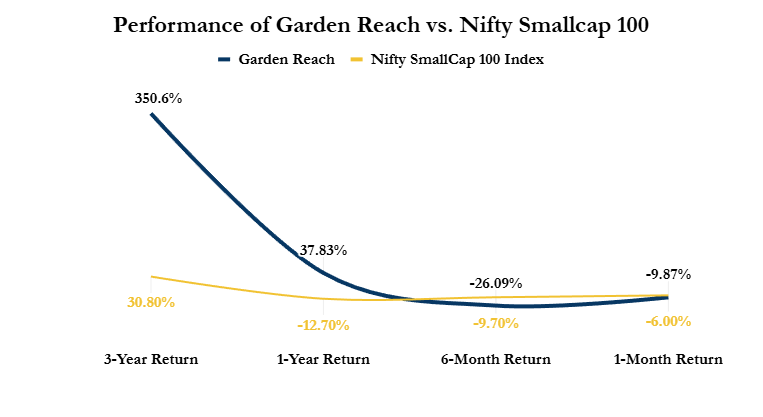

Performance Comparison with Index

{kind=link}

Garden Reach Shipbuilders & Engineers (GRSE) has shown a clear divergence between short-term weakness and long-term outperformance. In the short term, the stock has underperformed the index, with sharper declines over 1 month (-9.87%) and 6 months (-26.09%), reflecting broader small-cap correction and stock-specific profit booking.

However, the long-term performance remains exceptional. Over 1 year, GRSE delivered a +37.83% return, sharply outperforming the index’s -12.70% decline. The contrast is even starker over 3 years, where GRSE generated a 351% return versus 31% for the Nifty SmallCap 100, highlighting strong structural growth and sustained investor confidence despite near-term volatility.

What lies ahead for GRSE?

- Management aims for 25-30% annual revenue growth in FY26, with no near-term slowdown. Existing defence programmes provide revenue visibility for the next 2-4 quarters, and management expects a spike-plateau-spike growth pattern over the medium term.

- The order book stands at RS 20,000 crore and is expected to grow sharply. Management is confident of crossing Rs 50,000 crore by the end of FY26, with potential upside to Rs 75,000 crore if the P-17 Bravo frigate programme is secured.

- The Next-Generation Corvette (NGC) order, where GRSE is L1, is expected to be finalized within FY26 and will be a major revenue and margin driver from FY27 onwards. P-17 Bravo is another large potential catalyst, supported by GRSE’s successful execution of P-17 Alpha.

- Ongoing projects ensure steady execution through 2026 and beyond, while smaller commercial, research, and export orders help bridge gaps between large defence programmes, reducing revenue volatility.

- Domestic non-defense PSU demand (207 vessels) represents a Rs 5,000 crore opportunity. Export momentum, led by Europe, continues with the 12 German multi-purpose vessel order.

- Shipbuilding capacity rises from 28 to 32 ships by 2026, supported by brownfield expansion in West Bengal. A greenfield West Coast yard (with a 3-4 year timeline) targets 40 concurrent ships to support large defence and commercial projects.

- The 30mm Naval Surface Gun provides scalable diversification, with 10 guns contracted, 7 under negotiation, and 50 under inquiry. Core shipbuilding margins are guided at 7.5%, with NGC expected to deliver higher-than-average margins.

Key metrics of competitors:

MetricsGarden Reach Shipbuilders & Engineers LtdMazagon Dock Shipbuilders LtdCochin Shipyard LtdMarket Capitalisation₹27,102.00₹100,223.00₹42,516.00Price-to-Earnings Ratio43.9742.9455.98Book Value200.42200.39219.41Dividend Yield %0.59%0.70%0.60%ROCE36.26%32.92%15.76%ROE26.85%26.19%13.33%Debt-to-Equity Ratio0.010.000.2Promoter Holdings74.50%81.22%67.92%FII Holdings3.26%1.97%3.22%DII Holdings1.99%5.65%6.48%Order Book20,20627,41521,100For a real-world comparison, GRSE is the efficiency champion, Mazagon Dock is the scale leader, and Cochin Shipyard offers volume but lower returns. GRSE, though much smaller with a Rs 27,102 crore market cap vs Mazagon’s Rs 100,223 crore, generates better returns on capital (ROCE 36.3%) than Mazagon (32.9%) and more than double Cochin (15.8%), showing superior execution. Profitability is similarly strong, with ROE at 26.9%, slightly ahead of Mazagon (26.2%) and far superior to Cochin (13.3%).

Valuation-wise, GRSE trades at a P/E of 44x, nearly identical to Mazagon (43x) and meaningfully cheaper than Cochin (56x), suggesting investors pay a fair price for its efficiency despite its smaller size. Financial risk remains low, as GRSE is virtually debt-free (D/E 0.01), in line with Mazagon and better than Cochin (0.20). While its order book of Rs 20,206 crore is lower than Mazagon’s (Rs 27,415 crore), it is comparable to Cochin (Rs 21,100 crore), making GRSE a high-return, compact operator rather than a volume-driven shipyard.

Conclusion:

GRSE is a high-efficiency defence shipbuilder with strong execution, superior returns on capital, and clear long-term growth visibility. Despite being smaller than peers, it delivers better profitability, near-zero debt, a solid order book, and exposure to India’s multi-decade defence and maritime upcycle, making it a quality long-term play rather than a short-term stock.

Disclaimer: The views and investment tips expressed by investment experts/broking houses/rating agencies on tradebrains.in are their own, and not that of the website or its management. Investing in equities poses a risk of financial losses. Investors must therefore exercise due caution while investing or trading in stocks. Trade Brains Technologies Private Limited or the author are not liable for any losses caused as a result of the decision based on this article. Please consult your investment advisor before investing.

{kind=link}

The post ₹20,000 Cr Order book and 36% ROCE : Why This Defence PSU Stock Deserves a Second Look appeared first on Trade Brains.

Related Articles

Why did KPIT Technologies share crash up to 29% in one month?

Synopsis: KPIT Technologies Limited shares fell nearly 29% in a month amid Europ...

Solar Industries, Caplin Point and 6 other stocks delivering back-to-back EPS growth

Synopsis: Stocks like Solar Industries, Waaree Energies, and Navin Fluorine and...

Will Max Financial share price cross ₹2,000 after announcing robust Q3 results?

Synopsis: Max Financial gains after robust Q3 performance; Jefferies reiterates...

Angel One Vs Groww: Which stockbroker performed better in Q3?

Synopsis: Angel One and Groww delivered contrasting performances in Q3 FY26. Ang...