Polymarket US Posts $256M March, Launches Politics and Is Built to Scale

Alex Smith

2 months ago

- ▸ Polymarket US recorded $255.9 million in notional trading volume in March 2026, including a high of $88.8 million the week of March 30.

- ▸ The platform launched its first political and economic markets on April 8 with many more imminent.

- ▸ Polymarket US is set to scale, with a market-best 1.25% fee cap, liquidity incentives, and a clear path to distribution partnerships.

Four months after its debut, Polymarket US has entered a full sprint to public launch. The platform is now moving fast, built on a CFTC-regulated exchange and clearinghouse, a fee structure that undercuts every major competitor, and a liquidity incentive program designed to scale. On April 8, it officially expanded beyond sports, dropping its first political and economic markets after filing 16 new contract certifications with the CFTC on March 31.

The timing follows its strongest month and strongest week on record. Polymarket US recorded $255.9 million in notional trading volume in March, with its catalog growing from 1,372 to more than 4,100 available markets in a single calendar month. The week of March 30, spanning the Final Four and the start of the MLB season, came in at $88.8 million, the platform’s highest weekly volume to date, according to our internal data tracking.

The infrastructure to handle what comes next is already in place. What isn’t in place yet is the full public launch, though that’s clearly imminent.

Polymarket US adds politics and economic markets

On March 31, Polymarket filed 16 new contract certifications with the CFTC in a single batch, the required regulatory step before any new market category can go live. The first markets of the batch to go live first appeared Wednesday morning and included:

- Fed decision in April

- CPI year-over-year in April

- U.S. House Midterm winner

- U.S. Senate Midterm winner

Many more markets are expected to drop in the coming hours and days. The March 31 filing covered:

- 5 election and political contracts (with 2026 midterm primaries already underway)

- 3 macroeconomic contracts (Fed rate decisions, GDP, CPI)

- 2 AI-native market types

- 3 entertainment contracts

- sports props contract

- crypto price contract

- weather contract

Notably, Polymarket already had liquidity incentives listed for political markets in early April, readying the infrastructure and incentives to seed order books before contracts were live. According to published documentation, every eligible politics market has $5,000 per day set aside in liquidity rewards, split proportionally among market makers quoting those markets.

What is Polymarket US?

Polymarket US is a legally distinct product from Polymarket Global, a blockchain-based exchange that rivals Kalshi in terms of trading volume and popularity. Polymarket’s two platforms run separate order books, operate under different regulatory frameworks, and are in two different universes when it comes to volume and scale.

Polymarket US is operated by QCX LLC, a CFTC-regulated Designated Contract Market built on the $112 million acquisition of QCEX in fall 2025. It received its CFTC Amended Order of Designation on November 25, 2025, and launched its app days later. You fund it with a debit card, Apple Pay, ACH bank transfer or wire transfer, with no crypto wallet needed. Trading runs nearly 24/7, with a brief Tuesday morning maintenance window.

Polymarket US operates as a Central Limit Order Book (CLOB), and uniquely, it runs both the exchange and the clearinghouse. The QCEX acquisition brought two CFTC-registered entities under the Polymarket umbrella: QCX LLC (the DCM, or exchange) and QC Clearing LLC, operating as Polymarket Clearing (the DCO, or clearinghouse). Under CFTC Letter No. 25-48, all contracts on the platform clear directly through Polymarket Clearing, no third-party clearinghouse involved. When two orders match, Polymarket Clearing steps in as the central counterparty to both sides, guaranteeing settlement. All positions are required to be fully collateralized: the clearinghouse holds sufficient funds to cover the maximum possible payout on every open contract at all times.

March Madness jumpstart

After nearly three months of slow rollout, Polymarket made a major push for March Madness that paid off. The platform had been adding market types steadily since launch: NBA, college basketball, UFC, then spreads and totals, then international soccer and tennis. But March was where the catalog and the calendar finally aligned.

The exchange paired an aggressive marketing strategy with a stress test of its liquidity incentive program. Polymarket sent frequent push notifications to existing customers, highlighting key upcoming NCAAB matchups and structural advantages of trading on the exchange model compared to a sportsbook. In particular, popups highlighted the absence of “lockouts,” “best payouts in the world,” and ability to cash out before market resolution. Here’s a sampling:

The March Madness run also gave a first real look at how Polymarket scales liquidity incentives for high-profile events. Every NCAA Tournament game carried $100,000 in total liquidity rewards, split between $2,500 early, $17,500 day-of, and $80,000 live, with the heavy weighting toward in-game periods designed to keep the order book tight when trading volume (and volatility) peaks. Spreads and totals markets carried their own reward pools layered on top. Futures and qualifier markets (Sweet 16 through the title game) got bumped from $5,000 to $10,000 per day mid-tournament on March 24, a signal that Polymarket was actively tuning the program in real time as the bracket thinned.

Polymarket US by the numbers

The results were promising. For the first two weeks of March, the platform was running at roughly $30 million per week. That could be considered healthy for a sports-only platform just four months old, but not necessarily a breakout. Then the college basketball postseason began in mid-March, and weekly volume jumped 173% in a single week and kept climbing from there.

Polymarket US Weekly Volume

PNG Embed CSV Share Polymarket US Weekly Volume week_start Notional Volume # of Markets 2/23/2026 $31,251,123 602 3/2/2026 $30,454,603 583 3/9/2026 $29,170,328 899 3/16/2026 $79,587,159 1,044 3/23/2026 $84,146,451 1,076 3/30/2026 $88,766,605 1,562 (function() { function _ptmInit() { var el = document.getElementById('ptm-chart-1'); if (!el) return; var ctx = el.getContext('2d'); new Chart(ctx, { type: 'bar', data: { labels: ["2\/23\/2026","3\/2\/2026","3\/9\/2026","3\/16\/2026","3\/23\/2026","3\/30\/2026"], datasets: [{"label":"Notional Volume","data":[31251123,30454603,29170328,79587159,84146451,88766605],"backgroundColor":["#1E90FF","#1E90FF","#1E90FF","#1E90FF","#1E90FF","#1E90FF"],"borderRadius":4,"maxBarThickness":64}] }, options: { responsive: true, maintainAspectRatio: false, layout: { padding: { top: 8, bottom: 4 } }, plugins: { legend: { display: false }, tooltip: { backgroundColor: '#0f172a', titleFont: { family: "'Plus Jakarta Sans', sans-serif", size: 11, weight: 600 }, bodyFont: { family: "'Plus Jakarta Sans', sans-serif", size: 11 }, padding: { x: 10, y: 8 }, cornerRadius: 6, displayColors: false, callbacks: { label: function(ctx) { return ctx.dataset.label + ': ' + ptmCharts.formatValue(ctx.parsed.y, 'number'); } } } }, scales: { x: { grid: { display: false }, ticks: { font: { family: "'Plus Jakarta Sans', sans-serif", size: 11, weight: 500 }, color: '#8a90a0' } }, y: { beginAtZero: true, grid: { color: 'rgba(0,0,0,0.05)', drawBorder: false }, border: { display: false }, ticks: { font: { family: "'Plus Jakarta Sans', sans-serif", size: 11 }, color: '#8a90a0', padding: 8, callback: function(val) { return ptmCharts.formatValue(val, 'number'); } } } } } }); } if (typeof Chart !== 'undefined') { _ptmInit(); } else { document.addEventListener('DOMContentLoaded', _ptmInit); } })();Polymarket US didn’t manufacture volume through promotions alone, it captured real organic demand when large, liquid sporting events were available to trade. The March Madness test case showed a platform that could handle it. The NCAA Men’s Basketball Championship market on April 6 drew over $1.2 million in game-related markets. The futures Championship winner market brought another nearly $80K.

- Game winner: $820,672.58

- Spread: $266,797.57

- Total/O-U: $148,617.67

- All final-related markets combined: $1,236,088

- Championship winner (futures): $79,899

For context: Kalshi and Polymarket Global each set all-time monthly volume records in March, with $13.07B and $10.57B respectively. Polymarket US at $255.9M isn’t in the same conversation yet, understandably so. But it appears primed for a similar growth trajectory.

March top markets

March’s top 20 markets by volume were all basketball, including 13 college basketball game winner markets and seven NBA regular-season games, all game winner (moneyline) markets. The top market, Tennessee vs. Virginia on March 22, drew $3.6M. The first NBA game on the list, Atlanta vs. Detroit, ranked ninth. Polymarket US has been sports only since launch, but that is now changing.

Top 10 Polymarket US markets in March:

MatchupLeagueDateMarch VolumeTennessee vs. VirginiaNCAABMar 22$3,603,403Illinois vs. HoustonNCAABMar 26$3,213,405Iowa vs. ClemsonNCAABMar 20$2,815,743Vanderbilt vs. NebraskaNCAABMar 21$2,723,125Texas vs. BYUNCAABMar 19$2,709,286Saint Louis vs. GeorgiaNCAABMar 19$2,694,608St. John’s vs. KansasNCAABMar 22$2,629,940Iowa vs. FloridaNCAABMar 22$2,538,212Atlanta vs. DetroitNBAMar 25$2,504,625Golden State vs. DallasNBAMar 23$2,435,376Source: DeFi Rate Polymarket US database. Notional volume = total dollar value of positions across the market (both sides combined).

Why prices are better and how Polymarket US builds the book

The pricing advantage at Polymarket starts with fee structure. Traditional sportsbooks charge vig baked permanently into every line they offer, typically 4–5% on a standard market, invisibly extracted on every dollar wagered regardless of how confident the market is in an outcome. Polymarket US charges a trading fee calculated on price uncertainty with the following formula: p x (1 – p), where p is the trade price. Fees peak at a 50/50 market, a maximum taker fee of $1.25 per 100 contracts, and fall toward zero as outcomes approach near-certainty.

After the 50% weekly taker rebate, net cost works out to roughly 1.25% of trade value in the worst case. Makers, traders who post resting limit orders rather than taking existing ones, collect an additional 25% rebate at point of execution. The exchange earns only on matched volume and takes no position on outcomes.

The real-world result was visible in our March 24 house take analysis, where we tested live odds across six prediction market apps and two sportsbooks during five NCAA Tournament games. Polymarket US ranked first in every single game, by a factor of three or more against most of the competition. The reason comes down to a concept called overround.

On any sportsbook, if you add up the implied probability of every possible outcome (say, Team A wins and Team B wins), the total comes to more than 100%. A standard -110/-110 line implies each side has a 52.4% chance of winning. That’s 104.8% combined. The extra 4.8% is the sportsbook’s cut, baked invisibly into every line they post and is simply the price of playing.

On Polymarket US, prices are set by traders competing on the order book, not by the house. That means Yes and No prices tend to sum close to $1.00 (a fair market), with the exchange’s fee charged separately and disclosed explicitly on top. That fee, after the weekly taker rebate, works out to roughly 1.25% of trade value in the worst case, on a 50/50 market, and less as odds shift to the extremes. Our experiment put the effective overround advantage at three times or more compared to most competitors we tested.

Liquidity incentives and distribution pathways poised to scale

But better pricing only compounds when the order book is liquid enough to absorb real volume, which is where Polymarket’s liquidity programs come in. The Market Maker Incentive Program (effective January 27, 2026) pays active market makers who post resting limit orders continuously, using a quadratic spread-scoring function specifically designed to concentrate liquidity near the midpoint, where it matters most for price quality, rather than rewarding superficial depth.

The Liquidity Provider Program (filed March 3, 2026) works differently: approved LPs receive a fixed weekly stipend for maintaining two-sided quotes on assigned markets, functioning as a subsidy for thinner markets that can’t yet sustain variable-reward market makers. The volume incentive program adds a third layer, providing rebates tied to trading activity that benefit both market makers and active retail traders. March Madness games carried $100,000 in total liquidity rewards per game alone, front-weighted toward live periods when trading activity peaks.

The larger structural opportunity is the FCM and introducing broker pathway. The amended Order of Designation, which removed the prohibition on FCM intermediation, opens the door for registered futures brokers, fintech platforms, and introducing brokers to onboard their own customers directly onto Polymarket US. Polymarket’s rulebook defines a “Broker Participant” as any introducing broker, FCM, or similar entity with trading privileges on the exchange.

None of those partnerships are public yet, but the infrastructure is in place. When a major brokerage or trading app plugs into Polymarket US as a distribution channel, it will bring both retail flow and institutional market-making relationships with it, which is exactly what a young CLOB needs to reach the liquidity levels where the pricing advantage fully compounds.

State access: Almost all 50 states

Polymarket US is available in most of the country with one confirmed exception: Nevada. A state court issued a temporary restraining order in January following a lawsuit by the Nevada Gaming Control Board. Then a federal court in early March declined to move the case to federal jurisdiction, rejecting Polymarket’s argument that CFTC oversight preempts state gaming law. Nevada residents are currently blocked.

On April 2, the CFTC filed suit against Connecticut, Arizona, and Illinois, three states that had issued cease-and-desist letters to prediction market platforms, asserting exclusive federal jurisdiction under the Commodity Exchange Act. Those cases are ongoing.

Marching toward full public launch

Polymarket US is still currently in waitlist-only access, where new customers can use invite code RATE to gain access and receive a $20 credit for trading. As of April 8, it has its first political and economic markets to accompany a deep menu of sports, but no combos (parlays) yet.

The app received eight updates in March, more than in any prior month. One detail from the App Store version history: on January 30, six days after Nevada’s gaming board filed against the platform, Polymarket added “CFTC regulated” to every App Store impression. The designation is a deliberate legitimacy signal in an ongoing regulatory fight, and a key differentiator from its unregulated international platform.

The first serious stress test for Polymarket US is behind it. March Madness created the conditions for real volume, and the platform delivered. The week after March ended came in even stronger. The market certification filings from March 31 make clear the full public rollout and additional menu expansion is imminent. Soon, Polymarket will be available to all eligible US traders outside of Nevada, with a full slate of markets covering sports, politics, macroeconomic data, entertainment, AI, and crypto.

Following a successful testing phase, Polymarket US is set up well to compete and scale, with the lowest fees around combined with aggressive liquidity incentives to help ensure a smooth trading experience that keeps customers coming back.

Disclosure: DeFi Rate maintains an affiliate relationship with Polymarket US. This article reflects independent editorial analysis; the affiliate relationship did not influence our findings or conclusions.

The post Polymarket US Posts $256M March, Launches Politics and Is Built to Scale appeared first on DeFi Rate.

Related Articles

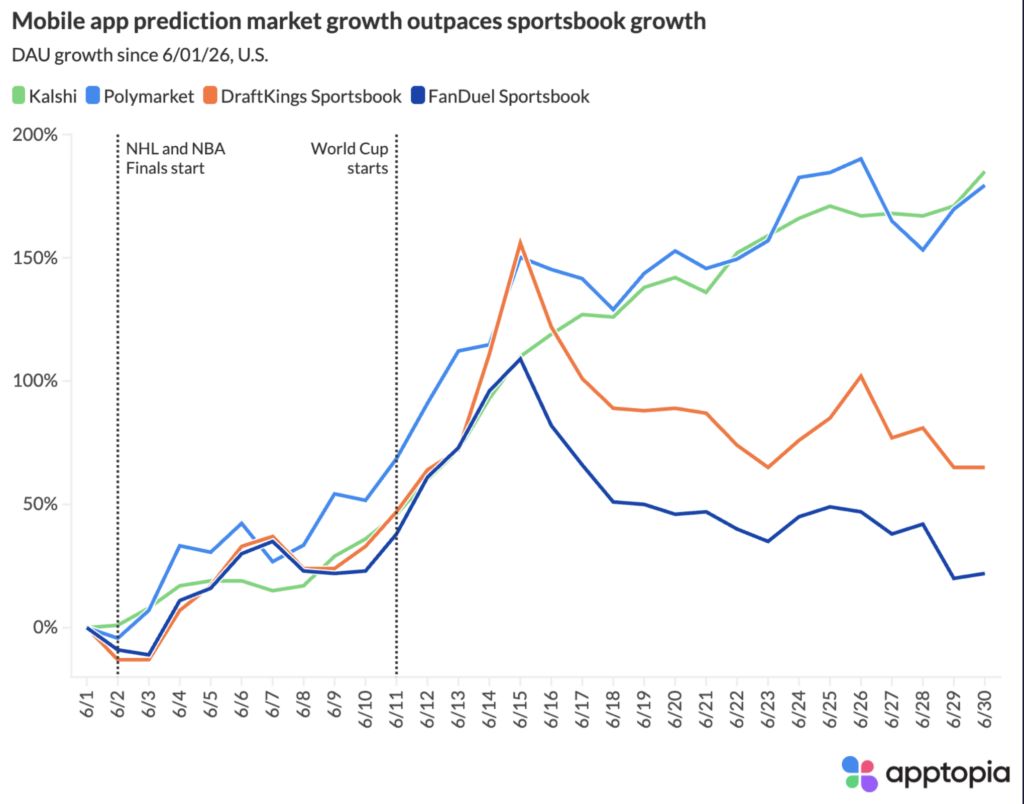

Kalshi Hits $1B on Winner Market as Prediction Sites Continue to Gain Daily Active Users During World Cup

Apptopia data shows prediction market apps continued adding users later in the W...

Kalshi Tops $7.5B With a Day Left, Smashing Its Own Weekly Volume Record

Kalshi has already surpassed $7.49 billion in notional volume for the week of Ju...

Referrals Are Live: Refer & Earn on Synthetix

Referrals on Synthetix are now live.Create & share your referral code and ea...

Novig Receives CFTC Approval as ProphetX Launches Sports Prediction Markets Days After Designation

Novig targets a summer rollout after earning CFTC designation, while ProphetX we...